Long Beach ADU Market Update: March 2026

Key Market Findings

Long Beach SB9 + ADU 2 bed 2 bath ADU in Long Beach with Separate Entrance

Long Beach is one of the more segmented ADU markets in Southern California right now. The entry-level and mid-range are behaving very differently from each other, and the gap between permitted and unpermitted properties is wider than it's been in over a year. Here's what the data looks like through March 2026 and what I expect through the second quarter.

Entry-Level Movement: Fast Sales With Strings Attached

Properties under $700K are moving quickly — some going pending within 10 to 13 days. But the speed is misleading if you don't look at what's actually selling. The fast-moving listings at this price point almost always involve unpermitted units, cash-only requirements, or both. These aren't mainstream buyer transactions. They're investor plays, and the buyer pool is narrow by design.

A $799K listing that sat for 113 days tells the other side of that story. Permitted, conventionally financeable, but overpriced relative to comps and in a neighborhood where buyers are more cautious. Price, condition, and permit status all matter at this level — not just the price tag. If you want to understand why permit status has this kind of impact on days-on-market, the financing dynamics that affect ADU buyer pools are worth understanding before you list.

Recent Closings Worth Noting

Two closings stood out in March. A La Marina Estates property sold for $2.695M in two days — cash, fully renovated, junior ADU included. That's a sharp transaction, but it's an outlier driven by condition and a specific buyer profile, not a signal about the broader market.

More representative was the Shipway Avenue Cliff May Rancho, which closed at its full asking price of $1.649M with conventional financing after 44 days. Permitted detached ADU, well-documented rental income, conventional loan. That's the product profile that's working in Long Beach right now.

A quadruplex in the Wrigley area told a more cautionary story — price dropped from $1.75M to $1.5M despite strong rental income. The problem wasn't the income; it was the appraisal. Fannie Mae's guidelines for appraising secondary dwelling units require documented rental history and income verification, and properties that can't produce that paperwork are getting hammered at appraisal. This is the same dynamic I broke down in a recent Long Beach pricing case study — when appraisers can't find the right comps, sellers pay for it.

Where Inventory Is Concentrated

Most of the active inventory sits in the $900K–$1.4M range. This is where you're seeing the most days-on-market variation as well. Correctly priced properties with documented rental income and conventional financing eligibility are moving in 25–40 days. Overpriced listings in transitional neighborhoods are sitting 75 days or longer and facing downward corrections.

The appraisal gap is a real issue here. Seller expectations in some neighborhoods are still anchored to 2024 pricing, and appraisers aren't meeting them there. Before pricing your property, it's worth running the same kind of comp analysis I walk through in Before You Build an ADU in Orange County, Check the Comps First — the methodology applies equally to sellers trying to establish a defensible list price.

What to Expect Through Q2 2026

Inventory in the $1M–$1.4M range will likely stay tight through June. Demand from owner-occupant buyers who want rental income from the ADU is consistent, and interest rates stabilizing in the mid-6s has kept that buyer pool active. I don't expect a wave of new listings — most sellers who were going to move have already moved.

The properties that will trade in this window are the ones that check three boxes: permitted detached ADU, documented rental income (ideally 12+ months of lease history), and pricing that the comps can actually support. Properties missing one of those three will either sit or trade at a discount.

Unpermitted units will continue to trade at a discount in the 10–15% range. That gap isn't closing anytime soon as lenders get more diligent about permit verification — California HCD's ADU compliance standards are the baseline lenders reference when a unit's permit status is in question.

For a comparison market, Fullerton's ADU inventory is showing a similar pattern — strong absorption on permitted detached units, extended days-on-market on anything with documentation gaps. Long Beach buyers are seeing the same dynamic play out.

Where I'd Focus as a Buyer Right Now

If you're shopping in Long Beach, the $1M–$1.4M range with a permitted detached ADU and documented rental history is the most financeable and most liquid product in the market. You're competing with a real buyer pool, but you're also buying something you can actually sell in three years without headaches. The value difference between detached and attached units is worth understanding before you narrow your search — the detached vs. attached breakdown for coastal Orange County applies closely to Long Beach as well.

If you're stretching toward the $1.4M–$1.7M range, make sure you have a lender who understands Fannie Mae's ADU income documentation requirements before you're in contract. Appraisal risk is real in that band right now.

If you own a Long Beach ADU property and want to know how your specific address sits against current comps, reach out. I'll pull the data and walk through the numbers with you.

Fullerton ADU Properties — Market Update (March 2026)

Overview

Four out of seven ADU properties already sold — that is strong absorption. The Fullerton market is showing healthy investor demand for multi-unit properties, with three additional listings still on the market.

This market analysis covers seven ADU properties currently tracked in Fullerton, representing a diverse range of price points and investor profiles across the market.

Sold Properties

128 S Citrus Avenue — $1,400,000 (Standout Investment Template)

This newly constructed 2025 home features seven bedrooms, four bathrooms, and was sold tenant-occupied with independent entrances — the investor's dream scenario. The property exemplifies the modern ADU investment model, with immediate rental income generating $575 per square foot.

This sale demonstrates strong market confidence in the ability to execute tenant-in-place strategies in Orange County — a critical advantage for investors seeking immediate cash flow.

Mid-Range Duplex Sales

Two duplex sales dominated the mid-range segment:

124 N Princeton Avenue — $1,100,000 (the list's lowest price point)

725 San Ramon — $1,449,000

Both represent turnkey cash-flow opportunities requiring no construction or significant repositioning. These sales underscore that Fullerton's duplex inventory appeals to buy-and-hold investors seeking immediate rental income without the development timeline.

Luxury Segment

660 Green Acre ($2.625 million on 20,700 square feet) illustrates the upper end of the Fullerton market. This property targets primary residence end-users rather than income-focused investors, signaling that Fullerton attracts diverse buyer profiles across all price tiers.

Active Listings

Three properties remain available in today's market:

1419 N Richman Knoll — $3.5 million asking price on 1.15 acres (the premium luxury segment)

Two modestly-priced options around $1.35 million (serving the entry-to-mid investor tier)

These active listings show continued pipeline strength, with new demand absorbing inventory quickly after close.

Market Insights: Why Fullerton Competes

Fullerton offers a lower entry point compared to coastal Orange County cities, with more duplex inventory and strong rental demand. The city's ADU regulatory environment continues to support development, positioning it as one of Orange County's most accessible markets for new investors.

The combination of moderate pricing, strong tenant demand, and a pipeline of qualified buyers makes Fullerton a strategic focus market for ADU investors in 2026.

Buena Park ADU Market Update: What Orange County Investors Need to Know (March 2026)

Buena Park doesn't come up in investor conversations as often as Anaheim or Costa Mesa, but that might be exactly why it's worth paying attention to right now. It sits at the intersection of Los Angeles County and central Orange County, which means tenant demand pulls from two directions. For investors focused on ADU properties in OC, Buena Park is quietly one of the more practical markets to be watching.

Buena Park 2 bed 2 bath ADU, 850 square feet with a separate entrance

Here's what the MLS is showing as of late March 2026.

Current Market Snapshot

Search criteria: Coming Soon, Active, Under Contract, and Sold within the last 60 days. Properties with confirmed ADU. Source: CRMLS Matrix, pulled March 29, 2026.

Average list price: $1,366,300

Average price per sq ft: $714

Price range: $1,199,900 to $1,550,000

Three properties. One already under contract. Tight inventory is the defining characteristic of this market right now.

What the Numbers Actually Mean for Investors

The El Prado property going under contract after 54 days is the most telling data point here. It sat longer than the others, likely because buyers were stress-testing the numbers at that price point. But it did go under contract, which confirms real demand exists even at the lower end of this range.

The two remaining actives are at 16 and 24 days. That's early, but that window closes fast when there are only two options in the city.

On the cash flow side, ADUs in this part of Buena Park are renting in the $1,500 to $1,800 per month range depending on size and finish level. On a $1.35M purchase with 20% down, your principal and interest is roughly $7,200 to $7,400 per month at current rates. An ADU generating $1,600 per month brings your effective carrying cost down to around $5,700 to $5,800. That's a real difference when you're evaluating how a property holds long-term.

The Buena Park Angle

One thing that doesn't show up in MLS data but matters for long-term hold value: Buena Park sits directly on the LA/OC county line. That geographic position means your tenant pool includes workers commuting in both directions, which keeps vacancy risk lower than in cities drawing from a single employment corridor. Proximity to the 5 and 91 freeways, Knott's Berry Farm, and the Buena Park Auto Center makes it genuinely accessible for working tenants, not just residents tied to one industry.

The homes themselves are mid-century stock, mostly built between 1948 and 1958 and updated or expanded in recent years to accommodate ADUs. That means the addition was likely done in the past decade. Worth confirming in escrow: verify permits with the City of Buena Park Planning Division, understand the rental history if the ADU has been occupied, and make sure the unit is on a separate meter or can be converted.

Under California state ADU law, most Buena Park properties qualify for ADUs, but the specific requirements and what "separate meter" means locally are items to nail down early in due diligence.

Who This Market Is Actually For

This is a market for investors already operating in OC who want exposure to a city with lower acquisition costs than the coastal markets but solid tenant fundamentals. The $1.2M to $1.55M range is real money, but compared to what ADU properties are trading for in Costa Mesa or Long Beach, Buena Park is a more accessible entry point with comparable cash flow potential.

If you're adding to an existing portfolio and looking for a market where the math is straightforward to model, Buena Park deserves a closer look. If you want to talk through whether a specific property here makes sense for your situation, that's exactly what the Seller Strategy Session at adurealtor.net/adusellers is designed for.

Thinking About Selling an ADU Property in Buena Park?

If you own a property here with an ADU and you've been watching the market, the data above gives you a baseline. But pricing an ADU property correctly isn't a standard residential comp pull. Buyers are factoring in rental income, permitting status, and ADU configuration alongside square footage. Getting that number right requires a different approach than a typical listing.

Start that conversation here: adurealtor.net/adusellers

Frequently Asked Questions: ADU Properties in Buena Park

Are ADU properties in Buena Park a good investment in 2026?

Based on current MLS data, Buena Park ADU properties are holding firm in the $1.2M to $1.55M range with tight price-per-square-foot consistency across listings. ADU rental income in this area runs $1,500 to $1,800 per month, which meaningfully offsets carrying costs on a typical purchase. Whether a specific property pencils depends on your financing structure and rent assumptions, but the market fundamentals are sound.

What is the average price of an ADU property in Buena Park right now?

As of March 2026, the average list price across current ADU-equipped listings in Buena Park is approximately $1,366,300, with a range of $1,199,900 to $1,550,000. Average price per square foot is $714 across the three active and under contract properties in this data set.

How much does an ADU add to home value in Buena Park?

In Buena Park's current market, ADU properties are trading at a premium over comparable single-unit homes. The size of that premium depends on the ADU's size, permit status, and income history. According to Fannie Mae's appraisal guidelines, ADU improvements must be valued separately and appraisers must demonstrate market acceptability through comparable sales analysis.

How do I find ADU homes for sale in Buena Park, CA?

ADU properties aren't always clearly labeled in standard MLS searches. Most require keyword searches in the remarks field for terms like "ADU," "guest house," "casita," or "junior ADU," or filtering by bedroom count and structure count. If you want a custom ADU search set up for Buena Park or nearby cities, reach out here: adurealtor.net/adusellers.

Is Buena Park ADU-friendly for new construction?

Buena Park falls under state ADU law, meaning most single-family lots qualify for at least one ADU and one JADU under California's ADU regulations. Specific setback, height, and size limits vary by zoning designation. If you're buying with the intent to add an ADU to a property that doesn't have one, that due diligence conversation should happen before you make an offer, not after.

What should I look for when buying an ADU property in Buena Park?

Start with permit history. A lot of ADUs in older Buena Park stock were added without permits, which creates liability and can affect financing options. Confirm permits directly with the City of Buena Park building department, verify the unit is on or can be converted to a separate meter, and review any existing rental history if the ADU is currently occupied. These are the items that move a deal forward or kill it in escrow.

ANAHEIM ADU MARKET UPDATE: MARCH 2026 — What Sellers Need to Know

Key Market Dynamics

The Anaheim ADU market is performing distinctly differently from the broader single-family home market. While standard residential properties face headwinds due to affordability constraints and selective buyer pools, properties with ADUs are experiencing stronger demand because they attract a different buyer demographic: investors.

This shift reflects broader changes in how lenders evaluate ADU properties. Fannie Mae's recent policy updates now allow secondary rental income from ADUs to contribute toward mortgage qualification, making these properties more attractive to buyers with long-term investment intentions.

Anaheim attached ADU 2 bed 2 bath, 900 square feet

Days on Market Disparity

The most telling metric is the stark difference in listing speed. Properties priced between $1M-$1.75M with clear ADU documentation and transparent lease terms sell within 25-35 days. By contrast, comparable properties with unclear, undocumented, or overpriced ADU situations linger for 80+ days. According to the analysis, "That gap isn't about location or condition. It's about how well the seller communicated the investment case."

This pattern mirrors what we're seeing across other strong ADU markets in Orange County. Investors demand proof—clear rent rolls, lease agreements, and financials—before committing capital.

Why Anaheim Attracts Investors

Several structural advantages make Anaheim particularly appealing for ADU investment:

Larger lot sizes (especially near the Garden Grove border) accommodate detached ADUs rather than cramped conversions, allowing for the full-sized units that Anaheim's ordinance permits

More accessible entry prices compared to coastal Orange County markets like Newport Beach or Costa Mesa

Better rent-to-price ratios that make financial metrics work for investor acquisition models

Anaheim's regulatory environment has also become more investor-friendly. California's state ADU policies established streamlined permitting, and Anaheim has implemented clear height allowances (up to 16 feet for detached units) and reasonable setback requirements that reduce development risk and timeline uncertainty.

Common Seller Mistakes

Listings sitting longest typically share three problems: marketing to wrong buyer demographics, failing to provide documented financial data, and pricing based on perceived value rather than income-supported valuations.

The most costly error? Overestimating what an ADU will command in rental income without backing it up with comparable rent data or actual signed leases. Professional investors run the numbers before scheduling a showing—no documentation, no offer.

Market Timing

The window for advantageous sales positioning is narrowing. Sellers moving within 60-90 days with proper documentation stand to capture the current premium while investor demand remains elevated. Those holding out for traditional buyer profiles will likely face extended holding periods and eventual price reductions.

Properties that clearly communicate their investment potential—clean tenant documentation, professional photography of rental units, and transparent financials—are consistently outperforming the market.

How to Show Your Orange County ADU with Tenants in Place: Complete Strategy Guide

Overview

Selling a tenant-occupied ADU requires balancing legal requirements, tenant cooperation, and buyer expectations. This comprehensive guide addresses the practical and legal considerations for successfully marketing properties with existing tenants.

Key Legal Requirements

California's 24-Hour Notice Rule

The state mandates 24 hours' written notice before entering a tenant-occupied home. Showings must occur during reasonable hours (8 AM–5 PM weekdays, 9 AM–5 PM weekends). Violations can result in tenant refusal of entry, code enforcement complaints, and delayed sales. Understanding these requirements is critical—many sellers don't realize that improper notice can derail an otherwise strong transaction.

For clarity on California tenant protections, refer to the California Department of Consumer Affairs which provides detailed guidance on landlord entry rights.

Pre-Listing Preparation

Before listing, meet directly with tenants to explain the sale and outline their options. The conversation should clarify whether they might be retained as tenants under new ownership or required to vacate. Documentation of this discussion protects both parties.

If your ADU is in a market like Anaheim or Costa Mesa, tenant communication becomes even more important given local market demand. Cities with stronger buyer interest often attract both owner-occupant and investor buyers, each with different expectations about occupancy.

Showing Strategy Options

Cooperative Tenants: Schedule individual showings with proper notice during agreed-upon windows.

Less Cooperative Tenants: Establish scheduled open houses with defined timeframes (e.g., "Saturday 10 AM–12 PM").

Limited Access: Drive-by showings significantly reduce qualified buyer pools and typically result in weaker offers.

Execution Best Practices

Provide written notice for each showing (email, text, or certified mail)

Request basic tidying before showings

Keep tours brief (10–15 minutes for ADUs)

Create a one-page showing guide detailing lease terms and maintenance history

Maintain documentation of all notices and showings

Consider showing services for complex situations

Addressing Buyer Concerns

Buyers typically ask about vacant delivery options, assuming existing leases, property condition, and tenant removal procedures. Transparency about lease terms, rent amounts, and California's 60-day vacancy notice requirement helps set realistic expectations.

Investor buyers especially want clarity on cash flow potential. If your property is valued similarly to other Orange County markets, showing strong rental income and lease stability can make your property stand out.

Timeline Considerations

Vacant properties close faster (30–45 days) and attract broader buyer pools at potentially higher prices. Month-to-month arrangements allow 60+ day closings; fixed leases benefit from listing 4–6 months before expiration. Investor buyers often prefer properties with stable tenant income.

Market-specific timing matters too. Long Beach and Fullerton markets show different buyer seasonality, so understanding your local demand curve helps time your listing strategically.

Conclusion

Success requires coordinating with tenants professionally, following California notice requirements strictly, and being transparent with buyers about lease conditions and occupancy options. With thoughtful preparation and clear communication, tenant-occupied ADUs can sell successfully to the right buyer—whether owner-occupant or investor.

The ADU Seller's Timeline: What to Expect From Listing to Close in Anaheim

Here's the full combined post:

The ADU Seller's Timeline: What to Expect From Listing to Close in Anaheim

If you own a home with an ADU in Anaheim and you're thinking about selling, you're probably wondering what the process actually looks like. How long does it take? What's different from selling a standard home? What do you need to prepare for?

The honest answer is that selling an ADU property in Anaheim is not the same as selling a regular single-family home — and sellers who treat it like one almost always run into problems. The buyer pool is different. The pricing strategy is different. The appraisal process is different. And the timeline has its own unique pressure points that can catch you off guard if you're not ready for them.

Here's a full breakdown of what to expect, from the moment you decide to sell to the day you close escrow.

Stage 1: Pre-Market Preparation (4 to 6 Weeks Before Listing)

This is the most important stage and the one most sellers skip. What you do before you hit the market determines everything that comes after — your price, your buyer pool, your negotiating position, and ultimately your final number.

The first thing to get clear on is your ADU's legal status. In Anaheim, ADU permitting has expanded significantly since California's 2020 legislation, but not every unit on the market is fully permitted and compliant. Before you list, you need to pull your permits and confirm that your ADU is on record with the City of Anaheim. An unpermitted unit doesn't automatically kill your sale, but it dramatically limits your buyer pool and gives buyers leverage to negotiate your price down. Know what you have before a buyer's inspector finds it for you.

Finally, decide on your tenant strategy. Are you going to market the property vacant or with tenants in place? In Anaheim, where investor activity is strong, a well-documented tenant at market rent can be a selling point for the right buyer. But below-market rent or an undocumented arrangement will work against you. Make the call intentionally, not by default.

Stage 2: Pricing and Listing Strategy (1 to 2 Weeks)

This is where most Anaheim ADU sellers get it wrong. Because there are still relatively few comparable sales of homes with ADUs on the MLS, pricing an ADU property correctly requires more than pulling comps. It requires building a case.

Your agent needs to price your home using a combination of approaches — nearby SFR sales adjusted for the ADU's contributory value, rental income data, and investor-grade metrics like gross rent multiplier and cap rate. If your agent is only pulling standard comps, they're leaving out the most compelling part of your property's value story.

Your listing itself needs to be written for your target buyer. In Anaheim, that's most often an investor or a multigenerational family. Lead with the income potential. State the ADU square footage clearly. Call out the permit status. Show the projected monthly rent for both units. A buyer scrolling Zillow or the MLS should be able to immediately understand what this property generates — not have to ask.

Professional photography of both units is non-negotiable. The ADU needs its own photos, not just a shot of the backyard. Buyers need to see the layout, the entrance, the kitchen, and the bedroom. If the ADU looks like an afterthought in the listing, it'll be treated like one in the offers.

Stage 3: Active Market and Showing Period (2 to 4 Weeks)

Once you're live, the showing period for an ADU property in Anaheim tends to attract a more specific buyer than a standard SFR listing. You're not going to get 40 families through on the first weekend. What you want are qualified, motivated buyers — investors who have done their homework, multigenerational families who have been searching specifically for this setup, and house-hackers who understand the income offset strategy.

This is why marketing matters as much as pricing. If your listing is reaching the right audience — investor networks, social media, targeted outreach — your showing period will be efficient. If it's sitting on the MLS with a generic description, you'll burn time and lose negotiating leverage.

During this stage, be prepared for buyers to ask detailed questions about the ADU. How is it metered — separate or shared utilities? What's the rental history? Is the tenant willing to stay or vacate? Has there been any deferred maintenance? The more prepared your answers are going in, the smoother this stage runs.

In a well-priced, well-marketed Anaheim ADU listing, you should expect offers within the first two to three weeks. If you're approaching four weeks with no serious activity, something is off — and it's almost always the price or the presentation.

Stage 4: Offer Review and Negotiation

Reviewing offers on an ADU property requires a different lens than a standard sale. Price matters, but so does buyer type and financing structure.

A cash investor offering slightly under asking with a 14-day close may net you more than a financed buyer at full price who needs 45 days and whose lender is going to order a conservative appraisal. A multigenerational family with a large down payment and flexible terms may be a better counterparty than an investor with a tight contingency window.

In Anaheim's current market, where days on market have been trending longer year over year, well-priced ADU properties that are positioned correctly are still generating strong offers. The sellers who struggle are the ones with stale listings who eventually accept whatever comes in. The sellers who win are the ones who created competition by doing the pre-market work correctly.

When negotiating, know your walk-away number before you're in the room. ADU properties often attract investors who are skilled negotiators. Having a clear sense of your minimum acceptable terms — price, contingency periods, possession date — keeps you in control of the conversation.

Stage 5: Escrow and the Appraisal (21 to 30 Days)

This is the stage that trips up the most Anaheim ADU sellers — especially those going with a financed buyer.

The appraisal on an ADU property is more complex than a standard SFR appraisal. Because comparable sales of homes with ADUs are still limited in many Anaheim neighborhoods, appraisers are often working with incomplete data. If your agent hasn't proactively prepared an appraisal package — documenting rental income, providing any available ADU comps, and making the income case in writing — you're leaving the appraiser to figure it out on their own. That almost always results in a conservative number.

A low appraisal doesn't automatically kill the deal, but it gives the buyer leverage to renegotiate. If the appraisal comes in below the agreed purchase price, you'll either need to reduce the price, have the buyer cover the gap in cash, or meet somewhere in the middle. None of those outcomes are ideal when you're 25 days into escrow.

The fix is to get ahead of it. Your agent should be in contact with the appraiser before they walk the property, providing a clear package that makes the income-producing case for your ADU's value. This is standard practice for commercial properties. It should be standard practice for ADU properties too — and most agents don't do it.

Beyond the appraisal, standard escrow items apply — title search, buyer inspections, any repair requests, and final walk-through. ADU-specific items to watch for include any inspection findings related to the ADU's electrical, plumbing, or egress that could raise compliance questions. If you addressed these in the pre-market stage, you'll sail through. If you didn't, this is where surprises show up.

Stage 6: Close of Escrow

In Anaheim, a smooth ADU sale from list date to close typically runs 45 to 60 days with a financed buyer, or as few as 21 to 30 days with a cash buyer — and that's by design, not a sign of a slow market. ADU properties sit at a higher price point and attract a smaller, more vetted buyer pool. You're not casting a wide net — you're waiting for the right buyer who understands the asset. Deals that drag significantly past 60 days are almost always dealing with an appraisal issue, a title problem, or a financing complication that could have been anticipated earlier in the process.

Once escrow closes, your responsibilities as a seller are largely done — with one exception if you have tenants. California tenant law requires proper notice and process for any change in tenancy, and Anaheim has its own local considerations around tenant rights. If your sale involved tenants in place, make sure the transition is handled correctly and documented. The last thing you want after a successful sale is a dispute with a former tenant.

The Bottom Line

Selling an ADU property in Anaheim is a real opportunity — but it rewards sellers who prepare and punishes those who don't. The timeline above isn't just a roadmap. It's a checklist of every place where the deal can go sideways and what to do to prevent it.

If you're thinking about selling your ADU property in Anaheim and want to walk through what your specific situation looks like — your unit, your tenant situation, your timeline — send me a DM on Instagram. I work exclusively with ADU properties across Orange County and I'll give you a straight answer on where you stand.

How to Sell a Home with an Unpermitted ADU in Orange County

If you have an unpermitted ADU on your property in Orange County, you're not alone. Garage conversions, backyard units, and add-ons built without permits are incredibly common across OC — especially in cities like Anaheim, Santa Ana, Garden Grove, and Fullerton where homeowners converted spaces to house family or generate rental income long before the current ADU boom.

The problem is that when it's time to sell, that unpermitted unit becomes a real obstacle. Here's what you need to know — and what you can do about it right now.

Why an Unpermitted ADU Hurts Your Sale

An unpermitted ADU creates problems at every stage of the selling process.

Appraisals. An appraiser can't count unpermitted square footage the same way they would a permitted unit. That doesn't mean it's worth nothing — a well-built unpermitted ADU with quality finishes, proper layout, and functional systems still carries value in the eyes of buyers. But the appraiser is limited in how they can credit it, which means you're leaving money on the table compared to what you'd get with a fully permitted unit.

Lending. Most lenders won't give full credit for unpermitted space. If your buyer is financing the purchase, the loan amount is based on the appraised value — which doesn't include your unpermitted unit. This limits what buyers can offer and still get their loan approved.

Disclosure. California law requires you to disclose known unpermitted work to potential buyers. That disclosure either scares off cautious buyers or becomes leverage for price reductions during negotiation. Either way, it costs you money.

Buyer pool. Owner-occupant buyers and conservative investors tend to walk away from unpermitted work entirely. They don't want the liability, the insurance risk, or the uncertainty. Your buyer pool shrinks to cash buyers and investors willing to take on the risk — and they'll price that risk into their offer.

The bottom line: an unpermitted ADU still has value — especially if it's a quality build — but you're not getting full credit for it. The gap between what your property could sell for with a permitted ADU versus an unpermitted one can easily be $100K to $200K+.

AB 2533 Changed Everything for OC Sellers

California's Assembly Bill 2533, effective January 1, 2025, created a legalization pathway specifically for unpermitted ADUs and Junior ADUs built before January 1, 2020.

Here's what makes it a game-changer for sellers:

Your city cannot deny your permit application just because the ADU was built without permits. That used to be the biggest fear — that applying to legalize would trigger enforcement, fines, or a demolition order. AB 2533 flips the script. Local agencies are required to work with you to bring the unit into compliance, not punish you for past work.

The review focuses on health and safety — not full code compliance. Your ADU doesn't have to meet every current building code. It just has to pass a Substandard Housing Inspection Checklist based on Health and Safety Code Section 17920.3. That means the city is looking for things like working smoke detectors, safe electrical, proper egress, and structural soundness — not whether your countertop height is to the inch.

No impact fees or penalties. As long as the unit doesn't require new utility infrastructure, the city cannot charge you impact fees, connection fees, or capacity charges for the retroactive permit. You pay standard permit and inspection fees — that's it.

Confidential pre-inspection. Before you even file with the city, you can hire a licensed contractor to inspect the unit privately. This gives you a clear picture of what needs to be fixed — without triggering any enforcement. You find out where you stand before you commit to the process.

Orange County's Development Services department has already set up a formal AB 2533 Safe ADU/JADU Legalization Program with published checklists and application procedures. This isn't theoretical — it's live and available right now.

How the Legalization Process Works

The process is more straightforward than most sellers expect.

Step 1: Get a confidential pre-inspection. Hire a licensed contractor to assess your unit. They'll identify any health and safety issues that need to be addressed before you go to the city. This is your risk-free first look.

Step 2: Gather your documentation. You'll need proof that the ADU was built before January 1, 2020. This can include old photos, property tax records, utility bills, real estate transfer disclosures, Google Earth satellite images, or even a signed declaration. You'll also need a basic site plan and floor plan showing the unit's layout and location on the property.

Step 3: Submit your permit application. File with your local building department — in unincorporated OC, that's OC Development Services. Include your documentation, the completed Substandard Housing Inspection Checklist from your contractor, and any required plans.

Step 4: City review and inspection. The city reviews your application with a focus on health and safety conditions. If they find issues during inspection, you'll be given a list of corrections — typically things like adding smoke detectors, upgrading electrical panels, or fixing egress windows. These are targeted fixes, not a full remodel.

Step 5: Complete corrections and get your permit. Once the required health and safety corrections are made and pass final inspection, your ADU is officially legalized. It now has a permit on record, gets its own city-assigned address, and becomes a fully recognized part of your property.

Your Two Options: Sell As-Is or Legalize First

This is where strategy matters. You have two paths, and the right one depends on market conditions, your timeline, and your budget.

Option 1: Sell As-Is in a Hot Market

Here's something most people won't tell you: if the market is hot — meaning properties in your area are selling in under 30 days on average — it may make more sense to list now and ride the momentum.

The legalization process through AB 2533 takes time. We're talking a few months at minimum between the pre-inspection, documentation, permit application, city review, corrections, and final sign-off. During that time, market conditions can shift. Interest rates can move. Buyer demand can cool. If you're sitting in a seller's market right now, waiting 4 to 6 months to legalize means you might come back to a different market — one where your property doesn't command the same price even with the permit in hand.

In a hot market, a well-built unpermitted ADU still carries real value. Buyers — especially investors — can see quality. A solid build with good finishes, functional systems, and clean layout communicates value even without the permit. You'll price it accordingly, disclose it properly, and attract buyers who see the upside. Some buyers will factor in the cost to legalize themselves and still make a strong offer because they want to lock in the property before someone else does.

This option works best when: the market is moving fast, your ADU is a quality build, and you don't have the time or budget to go through the legalization process before listing.

Option 2: Legalize Through AB 2533 — Maximum Value

If you have time and budget, legalizing your ADU before listing is the highest-ROI move you can make. A permitted ADU gets full credit in the appraisal — both the added square footage and the replacement cost of building that unit at today's OC prices ($350 to $500+ per square foot). That means an 800 sq ft permitted ADU could contribute $280K to $400K+ to your appraised value.

Legalizing also opens your property to the widest buyer pool. Financed buyers can get full loan value. Owner-occupants don't have to worry about liability. Conservative investors don't have to price in legalization risk. Everyone can offer with confidence, which means more competitive offers and a stronger sale price.

The cost to legalize through AB 2533 — permit fees, contractor inspection, and any required health and safety corrections — typically runs a fraction of the value it unlocks. For most OC sellers who have the time, this is the clear winner.

This option works best when: you have 4 to 6+ months before you need to list, the market isn't in a peak frenzy you'd miss by waiting, and you have the budget to cover permit fees and any required corrections.

How Do You Know Which Option Is Right?

This is exactly what we figure out together. Market timing, build quality, your financial situation, your timeline — it all factors in. There's no one-size-fits-all answer, which is why most generic real estate advice gets this wrong.

In a Seller Strategy Session, we'll look at current market conditions in your specific OC city, evaluate your ADU's build quality and permit status, and give you a clear recommendation: sell now or legalize first. Either way, you'll have a plan that's built around your situation — not a guess.

Not Sure Where Your ADU Stands?

Whether you sell as-is or legalize first, the answer starts with understanding your property, your market, and your options.

That's what we cover in a free Seller Strategy Session — your ADU's permit status, current market conditions in your city, and a clear recommendation on the best path forward for your situation.

How Is a Home with an ADU Valued When You Sell in Orange County?

It's the first question every ADU seller asks: How much does my ADU actually add to my home's value?

The short answer — a permitted ADU in Orange County can add $200K to $400K+ to your property's value. But the real answer depends on how the appraiser evaluates it, what paperwork you have ready, and how you position the property before you list.

Here's what you need to know before you list.

How Do Appraisers Value a Home with an ADU?

Appraisers use two primary methods. Most will use both and weigh them depending on the property.

The Comparable Sales Approach is the most common. The appraiser looks for recently sold homes nearby within the last 30-60 days within a half-mile radius that also have ADUs, then adjusts for differences in size, condition, location, and finish quality. The challenge in Orange County right now is that ADU comps are still relatively thin in some neighborhoods. If there’s not enough comparable sales, they often go back further in time. This is where having a knowledgeable agent matters — the right comps can swing your valuation by tens of thousands.

However, if the appraiser doesn’t have any comparable sales, they will then go to the Replacement Cost Approach. The appraiser looks at what it would cost to build that same ADU from scratch today — materials, labor, permits, everything at current prices. A benefit of this approach is when construction material prices increase in Orange County, your ADU is valued more. Building a detached ADU in OC today runs roughly $350 to $500+ per square foot depending on the city and finish level. If your ADU is already standing, permitted, and finished — you're essentially handing the next buyer something that would cost them six figures and 12+ months to replicate. That gets reflected in the appraisal.

Both Fannie Mae and Freddie Mac now recognize ADU rental income when qualifying buyers for loans. That means more buyers can afford your property, which means stronger offers when you sell.

Permitted vs. Unpermitted — This Is Where Sellers Lose Money

A permitted ADU shows up on the appraisal. An unpermitted one does not.

That's not a small detail. If your ADU doesn't have permits, the appraiser cannot count those square feet or that rental income in the valuation. Your buyer pool shrinks because lenders won't give full credit for unpermitted space. And California law requires you to disclose it — which either scares off buyers or invites steep price reductions.

If you have an unpermitted ADU built before January 1, 2020, California's AB 2533 created a legalization path that lets you retroactively permit the unit without penalties. Getting ahead of this before listing can be the difference between a $900K sale and a $1.1M sale on the same property. It's one of the first things we look at during a Seller Strategy Session.

What Documentation Should You Have Ready?

Buyers and their lenders are going to ask for this. Having it organized before you hit the market signals a clean, well-maintained property and speeds up escrow.

Gather your original building permits and final inspection sign-offs. Pull together any ADU-specific plans — architectural drawings, engineering reports, Title 24 energy compliance. Have proof of separate utility connections if applicable, and documentation of any rental income the unit has been generating. If you've made upgrades to the ADU since it was built, keep records of those too.

When an appraiser walks onto your property and sees a fully documented, permitted ADU with clear rental history, they have everything they need to justify the highest defensible value.

Two Buyer Pools — and Why That Matters for Your Price

Homes with ADUs in Orange County attract two distinct buyer types, and understanding both is key to pricing and marketing correctly.

Investors are evaluating the property as an income asset. They care about cap rate, cash flow, and the rent-to-price ratio. A well-documented ADU with strong rental income makes their underwriting easy — and easy underwriting means faster, stronger offers.

Owner-occupant families see the ADU as multigenerational living space, a home office, or future flexibility. Multigenerational buying hit an all-time high nationally, with 17% of recent home purchases involving multigenerational households. In OC, where housing costs push families to get creative, this number is even more relevant. These buyers pay a premium for a property that solves multiple needs under one roof.

Your listing strategy should speak to both. A one-size-fits-all approach leaves money on the table.

What You Can Do Right Now to Maximize Value

Before you list, focus on three things.

First, confirm your ADU is fully permitted and documented. This is non-negotiable for maximizing appraisal value. A permitted ADU gets counted in the valuation. An unpermitted one doesn't — full stop.

Second, understand what your ADU would cost to build today. That replacement cost number is your leverage. When construction costs in OC are running $350–$500+ per square foot, your existing ADU represents real, tangible value that a buyer would otherwise have to spend hundreds of thousands of dollars and over a year to create themselves. Know that number and make sure your agent does too.

Third, work with an agent who understands how ADU properties are valued, marketed, and positioned to attract the right buyers. Most agents treat a home with an ADU like any other listing. It's not. The pricing strategy, the marketing angle, the buyer targeting — it's all different.

Ready to Find Out What Your ADU Property Is Actually Worth?

Every ADU sale starts with the same first step: understanding your property's true value and building a strategy around it.

That's exactly what we cover in a free Seller Strategy Session — your property's ADU valuation, your best pricing approach, and a timeline that works for you.

Should I Sell My ADU Property Vacant or With Tenants in Place?

If you own a home with an ADU in Orange County and you're getting ready to sell, this is one of the first decisions you need to make — and most sellers don't think about it early enough.

Do you list it vacant? Or do you keep the tenants in place?

The answer isn't the same for every property. It depends on the type of home you're selling, who your ideal buyer is, and how much lead time you have before listing. Get this wrong and you're either leaving money on the table or creating a problem that delays your closing.

Here's how I walk my sellers through it.

The Two-Tier Framework for ADU Seller Tenant Strategy

I break this decision into two tiers based on the type of property you're selling. It's not complicated, but it makes a big difference in your final sale price.

Tier 1: Sell Vacant — Highest Price, Broadest Buyer Pool

If your property is a single-family home with an ADU in a residential neighborhood, you will almost always get the highest price by delivering it vacant.

Here's why. In a standard SFR neighborhood, your buyer pool includes families, owner-occupants, first-time investors, and experienced investors. That's the widest net you can cast. But the moment tenants are in place, you lose a huge chunk of that pool — because most families and owner-occupants don't want to buy a home where someone else is already living.

Vacant means more buyers competing. More competition means stronger offers. Stronger offers mean a higher sale price. It's that simple.

Tier 2: Tenants in Place — Narrows Your Buyer Pool, But Can Still Work for 3+ Unit Properties

If your property has three or more units — think SB 9 duplex with an ADU, or a triplex-style setup — having tenants in place isn't necessarily a dealbreaker. It's not an advantage. Let's be clear about that. It still narrows your buyer pool compared to selling vacant.

But for properties with 3+ units, the buyers who are looking at your listing are almost exclusively income-focused investors. They expect tenants. They're underwriting the deal based on the rent roll. And they're less likely to ask for vacant delivery because they want the cash flow from day one.

So it's not that tenants help you — it's that they hurt you less on a multi-unit income property than they would on a standard SFR with an ADU.

That said, the tenants still need to be paying market rent on solid leases for this to even be a conversation. If they're on month-to-month, paying below market, or creating any kind of management headache, that gives investor buyers a reason to offer less — not more. Below-market tenants on a multi-unit property aren't a selling point. They're a discount.

Why Most OC Sellers with ADUs Should Default to Vacant

Here's the reality for most of the ADU sellers I work with in Orange County: the majority of ADU properties in OC are single-family homes with a detached ADU in a residential neighborhood. They're not positioned as apartment buildings or multi-unit income assets. They're homes.

And for homes, vacant wins.

When a family walks through your property and sees someone else's furniture in the ADU, someone else's car in the driveway, and knows they'd have to navigate a tenant situation before they can use the space — that's friction. Friction reduces offers.

When an investor walks through and sees the same thing, they're calculating whether the current rent justifies their purchase price. If the tenant is paying under market or on a shaky lease, the investor discounts their offer to account for the risk.

Either way, tenants in a standard SFR neighborhood typically cost you money on the sale — not make you money.

Know the Notice Rules Before You Do Anything

Before you make any moves with your tenants, you need to understand how California notice requirements work. This is where sellers get tripped up the most.

Month-to-month tenants are the easiest to work with. There's no lease to wait out, no expiration date to plan around. You just need to give proper written notice:

30 days' notice if the tenant has lived there for less than one year.

60 days' notice if the tenant has lived there for one year or more.

That's it. Straightforward, predictable, and easy to plan around — as long as you do it early enough.

Fixed-term leases are a different story. If your tenant is on a lease that runs through, say, next October — you have to respect that lease. You can't force them out before the lease term ends just because you want to sell. The lease survives a sale, which means if you close with a tenant on a fixed-term lease, the new buyer inherits that lease and becomes the landlord.

This is why lease timing matters so much when you're planning to sell. If your tenant's lease expires in 4 months and you're not listing for 5, the timing works perfectly — give notice at the right point and the property is vacant by listing day. If the lease doesn't expire for another 14 months, you've got a harder decision to make about whether to wait, negotiate an early termination, or sell with the tenant in place.

The bottom line on notice: month-to-month gives you flexibility. Fixed-term leases require you to plan around the calendar. Either way, the earlier you look at this, the more options you have. The sellers who get stuck are the ones who didn't check the lease until after they decided to list.

The Complication I See Most Often: Buyer Wants It Vacant, But the Seller Can't Get the Tenant Out in Time

This is the scenario that causes the most stress, and it usually happens because the seller didn't plan early enough.

Here's how it plays out: the property hits the market, a strong offer comes in, and the buyer says "I want the property delivered vacant at close of escrow." The seller agrees — then realizes the tenant has rights, requires proper legal notice, and the timeline doesn't line up with the closing date.

Now you're in a tough spot. The buyer is frustrated. The tenant is caught off guard. The deal is at risk of falling apart or getting delayed. And the seller is stuck in the middle wondering how this got so complicated.

This is completely avoidable if you start the tenant conversation early.

This is exactly why the notice rules above matter. If your tenant has been there over a year, you need 60 days — and that's assuming they're month-to-month. If they're on a fixed-term lease, you might be waiting months for it to expire. You can't shortcut this. The law is the law.

This is one of the first things I work through with my sellers — well before we ever list the property. We look at the lease terms, check how long the tenant has been there, calculate the required notice period, and build a plan so that by the time we're accepting offers, the tenant situation is already handled. No surprises. No delays. No deals falling apart.

Your Action Steps Before Listing an ADU Property with Tenants

Don't wait until you're ready to list to figure this out. Here's exactly what to do and when:

6 Months Before Listing: Make the Decision

Decide now whether your property is a Tier 1 (sell vacant) or Tier 2 (tenants may stay for 3+ unit income property). If you're not sure, talk to an ADU specialist. The answer depends on your property type, neighborhood, and who your ideal buyer is. Getting this wrong wastes months.

4-5 Months Before Listing: Start the Tenant Conversation

If you're going vacant, this is when you begin the process. Review every lease — check the term, the expiration date, and whether it's month-to-month or fixed. Then give proper legal notice in accordance with California law. Don't guess at the timeline. Get it right the first time so there are no delays when it matters.

If you're keeping tenants in place for a Tier 2 sale, this is when you audit the rent. Are they paying market rate? If not, consider raising rents to market before listing so investor buyers see a strong rent roll — not a discount opportunity.

2-3 Months Before Listing: Get Your Paperwork Together

Gather everything a buyer and their lender will ask for: building permits, Certificate of Occupancy for the ADU, floor plans, utility records, current leases, and rent payment history. If anything is missing, this is the time to track it down — not during escrow when it holds up your closing.

1 Month Before Listing: Confirm Vacant Delivery or Finalize Rent Roll

If going vacant, confirm move-out dates are locked in and coordinate any cleaning, touch-up repairs, or staging. If keeping tenants, make sure every lease is current, signed, and presentable. Prepare a clean rent roll document showing tenant names, unit, monthly rent, lease term, and payment history. This is what investor buyers want to see on day one.

Listing Day: Have the Strategy Already Handled

By the time your property hits the market, the tenant situation should be a non-issue — not a negotiation point. Vacant properties should be empty, clean, and show-ready. Tenant-occupied income properties should have a polished rent roll and current leases ready to hand to serious buyers immediately.

The sellers who get the best results aren't the ones who figure this out after an offer comes in. They're the ones who had a plan months before the sign went up.

The Bottom Line

For most ADU property sellers in Orange County, vacant is the play. It gets you the highest price, the broadest buyer pool, and the cleanest transaction. The path to getting your property delivered vacant is straightforward — month-to-month tenants just need proper 30 or 60 day notice — but you have to plan ahead.

For 3+ unit income properties, tenants in place don't kill the deal — but they do narrow your pool to investor buyers only. Make sure rents are at market and leases are solid, or you're handing buyers a built-in reason to discount their offer.

Either way, the worst thing you can do is list without a tenant strategy. That's how deals fall apart.

Dylan Serna is an Orange County Realtor (DRE# 02217359) with eXp Realty specializing in ADU and investment real estate. Learn more at adurealtor.net.

Why Your ADU Property Isn't Selling in Orange County (And How to Fix It)

You have a home with an ADU in Orange County. You've listed it. And it's sitting.

That's frustrating — especially when you know what you have. An ADU property in OC is one of the most sought-after assets in today's market. Rental income, multigenerational living, investor demand — the fundamentals are strong. So why isn't it moving?

In most cases, the answer isn't the market. It's the approach. Here are the three most common reasons ADU properties stall in cities like Anaheim, Costa Mesa, Fullerton, Santa Ana, Garden Grove, and Orange — and exactly what to do about it.

Reason #1: It's Priced Like a Standard Single-Family Home — Because Nobody Really Knows How to Price It

This is the core problem, and it runs deeper than most sellers realize.

ADUs are still relatively new to the market. California only began aggressively streamlining ADU permitting laws in 2020, which means there simply aren't enough sold comparables yet to establish a reliable pricing baseline in most Orange County neighborhoods. Because few homes with legally permitted ADUs have been sold, appraisers and agents face a significant shortage of comparable sales to work from. That lack of data creates a pricing vacuum — and in that vacuum, most agents default to the nearest thing they know: standard SFR comps.

The result is a price that underrepresents what the property actually is.

This plays out across OC constantly. In Fullerton and Anaheim, where larger lots have made ADU construction more common over the past few years, sellers are coming to market with fully permitted, income-generating units — and getting priced as if the ADU barely exists. In Costa Mesa and Santa Ana, where investor demand for rental properties is strong, the same problem shows up: the listing doesn't reflect the income story, so the buyers who would pay full price never bite. In Garden Grove and Orange, where multigenerational households are common and ADU demand is real, sellers are leaving money on the table simply because their agent didn't know how to build the valuation case.

Here's where it gets worse. When there are no nearby ADU comps to pull, appraisers are forced to get creative. If there are no ADUs within a one-mile radius, that search radius must be expanded and adjusted to compensate for neighborhood price differences — a process that introduces estimation, not precision. And when appraisers do try to factor in the ADU's value using square footage, the math often falls apart. Simply multiplying ADU square footage by the main home's price per square foot can produce results that are wildly off from what real buyers would actually pay.

This is why you see ADU properties sit. They get listed at a price that reflects what the seller knows the property is worth — but without comps to support it and without an agent who knows how to build the income case, the listing goes stale. Price reductions follow. Then expired listings. Then relisting months later with a different agent and the same underlying problem.

The fix isn't to price lower. It's to price correctly — and that means building a valuation argument around rental income, gross rent multiplier, and cash-on-cash return, not just square footage and nearby SFR sales. That's the language investors speak, and investors are your most likely buyer at full price.

Reason #2: You're Marketing to the Wrong Buyer

ADU properties attract a specific type of buyer — and marketing to the general public the same way you'd market a standard home is one of the fastest ways to generate low-quality leads and weak offers.

There are three main buyer profiles for ADU properties in Orange County right now. First, the investor — someone looking for cash flow, portfolio growth, or a value-add opportunity. Second, the multigenerational family — parents and adult children who want to live together but separately. Third, the house-hacker — a primary buyer who plans to live in one unit and rent the other to offset their mortgage.

Each of these buyers has different motivations, different financing needs, and different things they want to see in a listing. This is especially true across OC's diverse cities. In Santa Ana and Garden Grove, multigenerational buyers are a dominant force — families looking for a setup where grandparents, parents, and adult children can share a property without sharing a front door. In Fullerton and Costa Mesa, you're more likely to attract the house-hacker — a younger buyer who wants the ADU rental income to help qualify for and carry the mortgage. In Anaheim and Orange, investors looking for turnkey cash flow are actively searching, but they need the numbers presented clearly to make a move.

A one-size-fits-all MLS description and a Zillow post isn't going to reach any of them effectively. If your listing isn't specifically calling out rental income potential, ADU square footage, permit status, and unit configuration — you're invisible to the buyers who matter most.

The fix: Your listing needs to be built for your target buyer. Lead with the income story. Show the numbers. Make it easy for an investor or a multigenerational family in Anaheim, Costa Mesa, or Fullerton to immediately see themselves in the property.

Reason #3: The Tenant Situation Is Killing Your Deal

This one is underrated and it catches a lot of sellers off guard. Who is in your ADU — and under what terms — has a direct impact on who will buy your home and how much they'll pay.

If you have a tenant paying below-market rent on a long-term lease, you've just eliminated a huge portion of your buyer pool. Owner-occupants who want to move family in can't. Investors doing the math on cash flow will see a problem immediately. Buyers relying on projected rental income to help qualify for their loan may not be able to use those numbers if the current lease doesn't support them.

This plays out differently depending on where you are in OC. In Santa Ana and Garden Grove, below-market long-term tenants are common — and sellers often don't realize how much that's suppressing their offers until they're already in escrow dealing with a lowball appraisal or a buyer walking away. In Anaheim and Fullerton, where investor activity is higher, a tenant in place can actually be a selling point — but only if the rent is at or near market rate and the lease terms are clean and documented. In Costa Mesa and Orange, where the buyer pool skews toward owner-occupants and house-hackers, a vacant ADU often generates the strongest offers simply because it gives buyers flexibility.

On the flip side, a vacant ADU opens the door to the widest possible buyer pool and removes any uncertainty around income assumptions. If you do have tenants in place, the situation can still work — but it needs to be the right tenants, at market rent, with clean documentation. That's a selling point. Below-market, long-term, undocumented tenancy is not.

The fix: Before you list, get clear on your tenant situation and build your strategy around it. Vacant gives you flexibility. Tenants in place can be an asset — but only when the numbers and the paperwork are clean.

The Bottom Line

An ADU property that isn't selling usually has nothing wrong with it. The issue is almost always pricing, positioning, or tenant strategy — three things that are entirely fixable before you ever go back on the market.

Whether you're in Anaheim, Costa Mesa, Fullerton, Santa Ana, Garden Grove, or Orange, the sellers who get top dollar are the ones who approach this asset class strategically — not the ones who list it like a standard SFR and hope for the best.

If your listing has gone stale or you're thinking about selling and want to do it right the first time, let's talk. I work exclusively with ADU properties across Orange County and I'll tell you exactly where your current approach is costing you.

Book a free seller consultation at adurealtor.net.

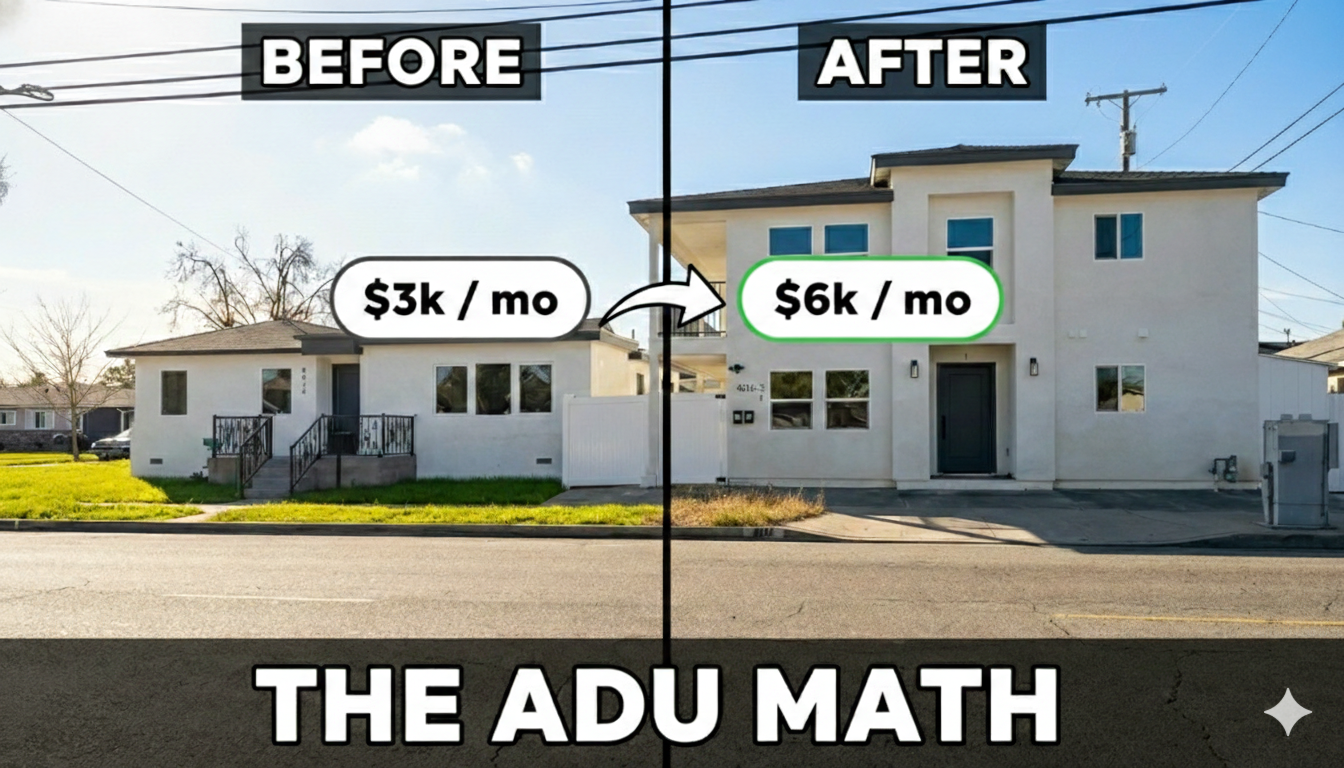

What Is My Home with an ADU Worth? How Orange County Sellers Can Price It Right

If you own a home with an ADU in Orange County and you're thinking about selling, the first question on your mind is probably: "How much is my home actually worth with this ADU?"

It's the number one question I get from sellers. And honestly, most people get the answer wrong — not because the information isn't out there, but because ADU properties don't get priced the same way as a standard single-family home.

Here's how it actually works, what mistakes to avoid, and how to position your property to sell for the most money possible.

How Are Homes with ADUs Valued in Orange County?

The most reliable method right now is comparable sales — looking at recent sales of similar properties with ADUs that have sold in your area, typically within a half-mile radius.

This is where it gets tricky. ADU properties are still relatively new to the resale market. In some neighborhoods, there might be three or four solid comps. In others, there might be zero.

When there aren't enough ADU comp sales nearby, appraisers will typically fall back on the replacement cost method — essentially asking: "What would it cost to build this ADU from scratch today?" That number gets added to the base home value.

Both methods are valid. But as a seller, the one that benefits you most depends on your specific property, your neighborhood, and how well your ADU is documented. That's where working with someone who specializes in ADU properties makes a real difference.

The Biggest Pricing Mistake ADU Sellers Make

Here's what I see over and over again: sellers overvalue the ADU because they spent a lot building it.

And honestly? I don't blame them. Not even a little.

If you've been through an ADU build, you know what it takes. The months of waiting on permits. The back-and-forth with contractors. Inspections that fail over something small and set you back weeks. The stress of managing a renovation while still living your life. By the time it's done, you're emotionally and financially invested in a way that's hard to put a number on.

So when it comes time to sell, it's natural to think: "I put $380K into this. I should get every dollar back and then some."

But that's not how buyers see it.

What you spent building the ADU is not the same as what it adds to your property's market value. Buyers aren't paying for your construction costs or your headaches — they're paying for what the property can do for them going forward. That means rental income potential, layout quality, permit status, and how the numbers work with today's interest rates.

A $380K ADU build doesn't automatically add $380K to your sale price. Sometimes it adds more. Sometimes less. It depends entirely on how the property is positioned and what comparable sales in your area support.

A Real Example: How the Numbers Work on an ADU Sale I'm Working Right Now

Let me break down a deal I'm currently working with so you can see how this plays out in real life.

My seller bought their property for $1,000,000 and put roughly $380,000 into the renovation and ADU build. That's about $1.38 million all-in. They still have about $300K left on the loan.

The property is now valued at approximately $1,550,000.

So let's do the math. After the remaining loan balance, the seller is walking away with roughly $1.25 million in proceeds — a delta of about $200K+ in profit on top of everything they put into it.

And I'll be honest — if you're in this seller's shoes, I know that $200K might not feel like enough. I get it. You dealt with months of construction. Permit delays. Contractor headaches. Inspections that didn't pass the first time. The emotional and financial weight of a full renovation plus an ADU build is real, and it takes a toll that doesn't show up on a spreadsheet.

Most sellers in this position want to list higher because of everything they went through. That's completely natural. But here's the hard truth: the market doesn't price based on your pain. It prices based on comps, income potential, and what buyers are willing to pay today.

If this seller tried to list at $1.6M or $1.65M because "that's what I need to make it worth it," the property sits. Days on market pile up. Price reductions follow. And ultimately they net less than if they had priced it right from day one.

The $200K delta is real equity. The dual-income structure means cash flow while holding. And the right pricing strategy — backed by comparable sales, not construction receipts — is what gets this deal closed at the strongest number the market will support.

What You Need to Know About ADU Appraisals in Orange County

Here's something most sellers don't realize until they're already in escrow: appraisers are known to exclude higher comps from superior-valued neighborhoods.

What does that mean for you? Let's say there's an ADU property that sold for a strong price two streets over — but it's technically in a more desirable pocket or a higher-valued neighborhood. An appraiser can (and often will) throw that comp out and use a lower sale from a more "comparable" area instead.

This is frustrating. Especially when you know your property is just as good or better than the one that sold higher. But appraisers are conservative by nature, and their job is to justify value within a tight radius of truly similar properties — not to stretch for the best number they can find.

This is why comparable sales within a half-mile radius matter so much. That's the zone appraisers are primarily pulling from. If the ADU sales in your immediate area are coming in lower than you expected, that's likely what your appraisal will reflect — regardless of what sold in the nicer neighborhood nearby.

As your ADU specialist, this is one of the first things I evaluate before we price your property. I pull every ADU comp within that half-mile zone, identify which ones an appraiser will actually use, and price your property so the appraisal supports the sale — not so we're fighting an uphill battle after an offer comes in.

What's Changed in 2026 That Affects Your Sale Price?

Two big shifts are working in your favor as a seller right now:

1. Buyers can now qualify for a mortgage using projected ADU rental income.

This is huge. In previous years, most lenders wouldn't count ADU rent toward a buyer's qualifying income. That meant fewer buyers could afford ADU properties, which limited your buyer pool.

Now, with updated lending guidelines, buyers can use the ADU's expected rental income to help them qualify for the loan. More qualified buyers = more competition for your property = stronger offers.

If your ADU has a documented rent history or a current lease, that makes the buyer's loan approval even smoother — which makes your property more attractive than one without income documentation.

2. More ADU comp sales are hitting the market, making valuations easier.

For years, one of the biggest challenges with selling an ADU property was the lack of comparable sales. Appraisers had to get creative, and that sometimes meant conservative valuations that didn't reflect the true income potential.

That's shifting. As more ADU properties trade in Orange County, the comp data is getting stronger. Appraisers have more sales to reference, and buyers have more confidence in what these properties are worth. If you've been waiting to sell, the data environment is better now than it's ever been.

How to Position Your ADU Property to Sell for Maximum Value

Pricing is only part of the equation. How you present the property matters just as much. Here's what I recommend to every ADU seller I work with:

Get your paperwork together first. Permits, Certificate of Occupancy, floor plans, utility records, and any rental agreements. Buyers and their lenders want to see that the ADU is legal, permitted, and documented. Missing paperwork creates hesitation during the offer period — and hesitation kills deals.

Know your buyer. Is your property best positioned as a family home with extra space, or as an income property for an investor? The answer changes your pricing strategy, your marketing, and who you target. A standard SFR with an ADU in a quiet residential neighborhood might sell best delivered vacant to a family. A multi-unit income property might sell best with tenants in place and a rent roll to show.

Don't price off your construction costs. Price off what the market supports — comp sales, rental income data, and what today's buyers are actually paying for similar properties. The market doesn't care what you spent. It cares what the property produces.

Work with someone who knows ADU properties. Most agents price ADU homes like regular single-family homes and leave money on the table. An ADU specialist knows how to highlight the income potential, target the right buyers, and make sure the appraisal supports the sale price.

Ready to Find Out What Your Home with an ADU Is Worth?

If you're thinking about selling your home with an ADU in Orange County, I can give you a realistic, data-backed valuation — not a generic Zestimate, but an actual analysis based on local ADU comp sales, current rent data, and what's happening in your specific market right now.

Schedule a free Timeline Roadmap Session and I'll walk you through what your property could sell for, the best strategy for your situation, and a personalized timeline so you're ready when the time is right.

Check out Our ADU Seller Guide

Dylan Serna is an Orange County Realtor (DRE# 02217359) with eXp Realty specializing in ADU and investment real estate. Learn more at adurealtor.net.

Why Fullerton Is One of the Best Cities in Orange County for ADU Investment Properties

If you're looking for an ADU investment property in Orange County, Fullerton should be at the top of your list. Here's why.

Lower Entry Price Than Most of OC

Fullerton has one of the lowest entry points for single-family homes in a desirable Orange County city. While the OC-wide median sits above $1.2 million, you can still find single-family homes in Fullerton starting in the high $800Ks to low $900Ks — especially in areas south of Commonwealth and near downtown.

That lower entry price matters because it means your all-in cost (purchase + ADU construction) stays manageable, and your numbers actually work from day one. In cities like Irvine or Huntington Beach, you're spending so much on the main home that the ADU income barely moves the needle. In Fullerton, the math is different — the ADU rental income can make a real impact on your monthly cash flow.

Corner Lots Create the Best ADU Opportunities

This is something most investors overlook, and it's one of the biggest advantages Fullerton offers: larger corner lots.

Many of Fullerton's older neighborhoods — particularly near downtown, along Harbor Blvd, and in the areas around Raymond Ave and Valencia — were built on generous lot sizes. Corner lots especially tend to have more usable space, better access for a separate ADU entrance, and more flexibility for placement and parking.

Why corner lots matter for ADUs:

More buildable area. Corner lots typically give you extra side-yard space that interior lots don't have, which means more room for a detached ADU up to 1,200 sq ft.

Separate access. You can give the ADU its own entrance from the side street, which tenants love and which justifies higher rent.

Better privacy. With the ADU facing a different street than the main home, both the homeowner and tenant get more separation — which means longer tenancies and less turnover.

Easier permitting. The extra footage on a corner lot often makes it simpler to meet setback requirements without needing variances.

I recently broke this down in a video on my Instagram — check it out here: Watch the Reel

The 3 Types of ADUs Explained (And Why Detached ADUs Usually Win)

https://www.youtube.com/shorts/vUueisZT310

If you’re starting from square one and trying to learn about ADUs, this is the easiest way to think about it. There are three main types of ADUs, and once you understand the difference between them, everything else starts to make more sense.

The first type is a Junior ADU. You don’t see junior ADUs as often because they’re harder to spot. A junior ADU is created by converting an existing part of the home, most commonly a portion of the garage. These units are limited to up to 500 square feet and usually work best when someone wants extra living space rather than a fully independent rental. Because they’re carved out of an existing structure, there are more layout and privacy limitations compared to other ADU types.

The second type is an attached ADU. Attached ADUs are built onto the main house and share at least one wall with the primary residence. You’ll typically see these used for multigenerational living, like parents living with family but still wanting their own space. They can work as rentals, but the shared structure usually means less separation and privacy compared to a detached unit.