ZA Memorandum No. 143: How to Put 4 Units on a Single-Family Lot in Los Angeles with No Lot Split

Most investors buying single-family homes in Los Angeles add one ADU and call it a day. They have no idea there's a City of LA planning memorandum that lets you put four units on that same lot — and that one of those units has no square footage cap.

It's called ZA Memorandum No. 143, and it's the best-kept secret in LA real estate investing right now.

What Is ZA Memorandum No. 143?

ZA Memo 143 is a City of Los Angeles planning directive that spells out the development standards for ADUs and JADUs in the city. It was updated to stay consistent with California's state ADU laws as amended through 2025, and it includes the combination tables that show exactly how ADUs interact with other housing types on a lot.

The part that matters is what happens when you combine an SB9 unit with an existing single-family home. Per the memorandum, that combination reclassifies the property as multifamily. And once it's multifamily, you unlock a completely different set of ADU allowances — including the ability to add two ADUs instead of one, with the state-mandated ADU carrying no size restriction.

That's the play.

The 4-Unit Formula

Here's how it breaks down on a single lot in the City of Los Angeles:

Unit 1: The existing single-family home. Your starting point. A standard SFR on a qualifying lot.

Unit 2: The SB9 unit. Under Senate Bill 9, you add a second primary unit to the lot. This is not an ADU — it's a full primary dwelling that gets appraised and valued the same as the original home. The moment this unit is on the lot, the property is now classified as a two-unit development. Per city code, that's multifamily.

This is where the magic happens. Once the lot is multifamily, ZA Memo 143's combination tables allow you to add two ADUs — a city ADU and a state ADU.

Unit 3: The city ADU. This is the ADU permitted under the city's local ordinance, subject to the city's standard size caps and setback requirements.

Unit 4: The state ADU. This is the California state-mandated ADU that every jurisdiction is required to allow on multifamily properties. Here's the kicker: the state ADU on a multifamily lot has no square footage cap. No size restriction. You can build it as large as the lot and setbacks allow. That means more bedrooms, more rent, and a dramatically better return than the single ADU most investors settle for.

The result: four income-producing units on one lot, with the state ADU potentially being the highest-grossing unit on the property because of its unrestricted size.

What This Looks Like on an Actual Lot Plan

LA lot plan designers like @lalotplans are already drawing these configurations. One common approach: convert the front attached garage into an ADU. Since it's attached to the main house, the SB9 unit creates a duplex on the lot. Now that the lot is multifamily, you place two ADUs in the rear — the city ADU and the state ADU — with parking laid out along the side. Four units, plenty of parking, and each one with functional separation so tenants feel like they have their own space.

This is not theoretical. These lot plans are getting approved and built in Los Angeles right now. The investors who know about ZA Memo 143 are the ones submitting them.

Real Numbers: What the Income Jump Looks Like

I've seen this play out in Lakewood and other LA County neighborhoods. Here's a real example from a property I evaluated:

A traditional single-family home was originally renting for $3,500 per month. The owner added an SB9 unit and ADUs. The property now generates $11,000 per month — more than three times the original income, on the same lot, without buying additional land.

That kind of income jump changes every metric that matters: cash-on-cash return, cap rate, and total property value. When appraisers value these properties, they use the income approach because comparable sales for SB9-plus-ADU properties are still limited. In Lakewood, I've seen these trading at roughly a 5.5 percent cap rate based on verified rent comps — not the inflated numbers listing agents put on the MLS.

Why the Multifamily Reclassification Is Everything

The reclassification from single-family to multifamily is the entire strategy. Without it, you're limited to one ADU on a single-family lot with standard city size caps. With it, you get two ADUs — and the state ADU has no size limit.

Two ADUs instead of one. On a single-family lot, you get one ADU. Period. Once the SB9 unit reclassifies the lot as multifamily, the combination tables in ZA Memo 143 open up the second ADU slot. That's an entire additional income stream that doesn't exist without the reclassification.

No square footage cap on the state ADU. This is the part most people miss. The state-mandated ADU on a multifamily property is not subject to the size restrictions that apply to single-family ADUs. You can build it as large as the site allows. On an oversized lot, that could mean a full three-bedroom unit generating rent comparable to the main home.

Better appraisal treatment. A four-unit property appraised under the income approach gets valued based on what it produces. If you're generating $11,000 per month in rent, the property's value reflects that income stream — not just what comparable single-family homes sold for down the street.

How to Check If Your Property Qualifies

Not every lot in LA qualifies for the full four-unit play. You need to confirm two things:

SB9 eligibility. Use ZIMAS to check whether the property meets the requirements under Senate Bill 9. The property must sit in a single-family residential zone (A1, A2, RA, RE, RS, R1, RU, RZ, or RW), be within half a mile of transit, and not fall within certain hazard or historic overlay zones. The ZIMAS checklist takes about sixty seconds — I wrote a full walkthrough on how to use ZIMAS to check SB9 eligibility if you haven't done it before.

Lot feasibility for four units. Even if SB9 checks out, you need enough lot area to physically fit all four units with code-compliant setbacks, parking, and access. Corner lots and oversized parcels above 6,500 square feet tend to work best. I always have my designer run a feasibility report during escrow so we know exactly what the site can support before we close.

The Two SB9 Paths — and Which One Gets You to 4 Units Faster

SB9 with lot split. You split the parcel and place the SB9 unit on the new lot. Requires you to intend to reside in one of the units for three years. Cities drag this out — plan on roughly a year. It's like the early days of ADU permitting when cities were still figuring out how to process applications.

SB9 without lot split. The parcel stays intact. You add the SB9 unit alongside the original home, then layer on the two ADUs per ZA Memo 143. About six months, no residency requirement, and the cleaner path to the four-unit configuration.

For most investors, the no-lot-split path is the better play. Faster timeline, no occupancy strings, same income upside.

What to Watch For

Timeline expectations. The SB9 unit alone takes around six months on the no-lot-split path. Add the ADU design and construction timeline — typically seven to twelve months — and you're looking at a twelve-to-eighteen month project from purchase to full income. Budget your reserves accordingly.

Rent verification. Listing agents routinely inflate projected rents on SB9 properties to support the price. Always pull your own comps. On the Hedda Street property in Lakewood, the listing projected $12,800 per month. My comps came back at $11,200 — a $1,600 per month difference that shifted the cap rate from 6.2 percent to 5.5 percent and knocked $80,000 off the realistic purchase price.

City-specific rules. ZA Memo 143 applies to the City of Los Angeles. If the property is in unincorporated LA County or a different incorporated city, the ADU combination rules may differ. Check LA County Planning's SB9 page for county-specific guidance.

Work with a lot plan designer who knows the play. Not every designer understands how SB9 reclassification opens up the two-ADU allowance. You want someone who has already gotten these four-unit configurations approved — designers like @lalotplans in LA are already drawing and getting these approved.

The Bottom Line

ZA Memorandum No. 143 is the playbook for turning a single-family lot in Los Angeles into a four-unit income property. The formula is: existing SFR plus SB9 unit makes it multifamily, which unlocks two ADUs — a city ADU and a state ADU with no size cap. That's four units on one lot.

The investors who already know this are generating three to four times the cash flow of a traditional single-family rental, on the same lots, in the same neighborhoods. They didn't find a secret market. They read the memorandum.

If you want help evaluating an SB9-plus-ADU play in Los Angeles, DM me on Instagram or download the ADU Buyers Guide to start running the numbers.

City of Orange ADU Market Update — May 2026

The City of Orange ADU market told a clear story this month: buyers are still paying premiums for the right ADU home, but they're getting picky at the top end. Eleven ADU-flagged properties hit the radar in early May — eight actives, two pending, and one closed sale that went $25,000 over asking after just seven days on market.

If you've got an ADU home in Orange you're thinking about listing this summer, or you're a buyer hunting Old Towne and Chapman-area income properties, this update is for you.

The Headline Numbers

Active inventory: 8 ADU-flagged single-family homes

Active price range: $1,425,000 to $1,995,000

Active median list: ~$1,732,000

Active price/sqft range: $491.59 to $859.98

Pending: 2 (both went under contract in 10–12 days)

Closed in last 30 days: 1, sold $25K over list in 7 days

Long DOM outlier: 264 days (yes, really — more on that below)

What's Active Right Now in Orange

Old Towne Orange + Chapman corridor (the hottest pocket)

This is where the action is. Four of the eight active listings cluster within walking distance of Chapman University and the Orange Plaza, and they're priced for the income-producing buyer pool more than the owner-occupant.

130–132 S Lime St — $1,699,900 (down from $1,799,900). 6BR/3BA two-on-a-lot. Front home from 1949 (extensively remodeled 2020), back ADU built in 2021, both move-in ready. List speaks to about a 4.78% cap rate at $9,000/mo combined rent. 44 days on market with a $100K reduction tells you the seller is open to offers.

417 N Citrus St — $1,695,000. 4BR front + newly built 2024 ADU (2BR/1BA, 749 sqft). Both currently leased ($5,960 front, $3,200 ADU). Combined gross $9,160/mo at a stated 4.9% cap. Tenant occupied through May 2026 (front) and May 2027 (ADU) — meaning a buyer steps into immediate cash flow but inherits the leases.

359 N Harwood — $1,799,000. Old Towne historic district Craftsman from 1925. Front 3BR/3BA, plus a 420 sqft 1BR/1BA upper-level ADU above the detached garage. ADU is rented. Charm + income.

246 N Stevens — $1,529,900. Mid-century 4BR home with a brand-new, never-lived-in 524 sqft ADU completed in 2025. Separate electric meter, fully permitted. Just hit the market April 28.

Cambridge / N. Tustin area (premium owner-occupant ADU homes)

634 E Adams Ave — $1,995,000 (down from $2,088,000). 5BR/6BA pool home with 683 sqft permitted detached ADU built 2022, plans for a 235 sqft expansion to 2BR. Solar, EV charging, wheelchair accessible. Currently licensed as a short-term rental. 58 days on market, $93K price drop — high-end Cambridge buyers are taking their time.

390 N Milford — $1,665,000. Two-story 5BR/4BA with a 462 sqft attached Junior ADU configured as a private in-law suite with gated entrance. Solar owned. 23 days on market.

Larger lots, off-Plaza

178 N Monterey Rd — $1,995,000. "Kibby House" — 4BR ranch on a huge 11,340 sqft lot, 13 blocks east of the Plaza. Has an 830 sqft "workshop/ADU/game room" with a 3/4 bath and vaulted ceilings — buyers should clarify the actual permit status. Notable: there's a $607,000 assumable VA loan at 2.25% that's making this property interesting to a niche buyer pool.

2929 E Hamilton Ave — $1,425,000. This is the long-DOM outlier. 3BR/3BA on an 8,856 sqft cul-de-sac lot with a fully upgraded 600 sqft 1BR/1BA private ADU (shared meters). On market since August 13, 2025 — 264 days. At this point it's a pricing problem, not a property problem. Worth watching for a meaningful reduction.

Pending Sales — What Buyers Just Locked Up

Two ADU homes went under contract in early to mid-April. Both deserve attention because they tell different stories.

1402 E Rose Ave — $1,549,000 (pending in 12 days)

5BR/3BA pool home in Old Towne with a fully permitted 426 sqft ADU at 1404 E Rose — converted in 2023, separate water and electricity meters, vaulted ceilings, tankless water heater. Permitted, separately metered ADUs are exactly what buyers are paying full ask for. Resort-style backyard with a new pool didn't hurt.

914 N Sacramento — $1,100,000 (pending in 10 days) — the AB 2533 story

This one's interesting. Mid-century home (originally built in Malibu, relocated to Orange in the 1970s — yes, really) with a 644 sqft detached ADU. The ADU is unpermitted, but the listing notes it "should qualify for the AB 2533 Safe ADU Legalization Program," and the buyer signed up anyway at $1.1M.

This is a real-time example of what I cover in detail in Selling a Home With an Unpermitted Garage Conversion or Bootleg ADU — buyers in 2026 are no longer running from unpermitted ADUs the way they did three years ago, as long as the seller is upfront and the path to legalization is clear. AB 2533 (effective January 1, 2025) made this much cleaner. If you have an unpermitted unit in Orange, the market just told you you can sell it — at a discount, with the right disclosures, to the right buyer.

Closed Sale of the Month: 2225 E Grove Ave

Listed $1,300,000. Closed $1,325,000. On market 7 days.

3BR/2BA Craftsman from 1960 with an attached 500 sqft Junior ADU (1BR/1BA, kitchenette without oven/stove). 8,000 sqft lot, 1,920 sqft of main house. Closed April 17, 2026 with conventional financing.

A few things to read into the data:

Permitted Junior ADUs still drive over-asking offers in Orange when the home is otherwise turnkey.

The buyer paid full freight even though the ADU kitchenette doesn't have a full stove (stays a JADU, not a full ADU).

$37,125 in seller concessions (mostly $33K to the buyer's broker fee). Net to seller approximately $1,287,875 — still over original list and a clean 7-day deal.

If you're wondering what your Orange home with an ADU could realistically sell for, this is the freshest comp in the cluster. I break down the full valuation framework in How a Home With an ADU Is Valued When You Sell.

What This Means If You're Selling an ADU Home in Orange

A few clean takeaways from this month's data:

Permitted, separately metered ADUs are the gold standard. The two pendings and the closed comp all share this trait. Shared-meter and unpermitted units sell — but at meaningful discounts.

Old Towne / Chapman-corridor income properties want a 4.7%+ cap to sell. If the math doesn't pencil, expect a price reduction or extended DOM.

The $1.6M–$2M Cambridge segment is taking its time. Two listings in this band have already cut price. If you're listing here, price tight and stage well — buyers have options.

Don't sit too long. The 264-day Hamilton listing is a cautionary tale. After 60 days without a contract, the market is telling you something. Listen.

What This Means If You're Buying

The under-$1.5M ADU home is rare in Orange right now. Sacramento at $1.1M is the only one — and it went pending in 10 days even with an unpermitted ADU. If your budget tops out below $1.5M and you want an ADU property, you'll likely need to look at unpermitted units, look at Anaheim or Garden Grove, or consider building one yourself.

Price reductions are happening above $1.65M. Don't rush at full ask in the upper tier.

Income-producing duplex-style ADU properties (Citrus, Lime) are sitting longer than vacant move-in homes — meaning more leverage if you actually want a tenanted property.

My Take Going Into Late Spring

May should bring more inventory in Orange — sellers who held off through Q1 are starting to list. I'd expect:

One or two more AB 1033 conversations to start leaking into listings as San Diego County's separate-ADU-sale activation continues to ripple through California's high-equity ADU markets.

Continued price compression at the top ($1.8M+) as buyers in this band stretch their search across more cities.

A pickup in Old Towne ADU activity as Chapman summer break reduces showing friction in tenant-occupied properties.

If you have an Orange home with an ADU and you're planning to list in 2026, the best thing you can do this month is get a real, current valuation — not a Zillow estimate, a real one. Reply to this post or book a 15-minute call and I'll send you the comp set within 24 hours.

For the broader OC picture, see my city of Orange ADU landing page and last month's April 2026 update.

Data pulled from the CRMLS on May 8, 2026. Listings, prices, and statuses change daily — verify before relying on any specific number. For California ADU rules and AB 2533 amnesty details, see the California HCD ADU page and the HCD ADU Handbook. For City of Orange permitting questions, contact the City of Orange Community Development Department.

Costa Mesa ADU Market Update: The Market Is Bifurcating Fast (May 2026)

If you read the March 2026 Costa Mesa update, you saw a market that was cooling at the top but still moving in the middle. Six weeks later, that gap has widened into a real split — and it's now the most important thing happening in Costa Mesa ADU real estate.

Here's what the May 2026 data is showing, pulled from three live data points across the city.

The closed comp: permits won, big.

934 Governor in Southwest Costa Mesa just closed on April 15 at $1,400,000 — $110,000 over the $1,290,000 list price, all cash, 12 days on market.

The existing home was a 2/3 1,848 sq ft 1954 build on a 7,350 sq ft lot. Nothing special on its own. The reason it traded over asking in under two weeks: approved plans and city permits in hand for a proposed 1,878 sq ft main residence (4 bed/4.5 bath) plus a 590 sq ft attached ADU plus a 2-car garage.

The buyer paid for the entitlement work. That's the whole story. Builders and investors are willing to pay a real premium when the permitting risk has already been eaten — because anyone who's gone through Costa Mesa Planning knows the timeline and uncertainty involved. If you own a Costa Mesa property and you're considering selling, this is exactly why permits-in-hand changes the comp conversation.

The active luxury listing: a $195K price cut tells the story.

1789 Nantucket Pl is still active at $2,995,000 — reduced from $3,190,000 on May 8. It's a 4 bed/4 bath, 3,250 sq ft 1991 home in a small gated community with Catalina views, fully rebuilt by the owner, with an attached ADU. The original list was $3,019,000 and it's now sitting at the bottom of its range after 24 days.

Translation: the top of the Costa Mesa ADU market — the $3M+ turnkey, ultra-finished, view-lot category — is not absorbing inventory at full price right now. The seller did the right thing by cutting early instead of letting it sit, but the cut itself is the signal. When luxury ADU product needs price reductions to attract attention, it's another data point on why ADU properties in OC are generally taking longer to sell than traditional product.

The pending listing: 92 days to find a buyer.

212 E 19th in Eastside Costa Mesa just went into contract on April 27 after listing on January 27 at an original $3,095,000. It dropped to $2,995,000 in March and finally found a buyer at that price — 92 days from list to pending.

This is a seriously high-quality property: 5/4 main home reconfigured by Abode Design + Build, plus a detached 2/2 938 sq ft ADU built in 2025, on an 8,100 sq ft Eastside lot in the Newport Harbor High School zone. Turnkey design, premium finishes, detached new-construction ADU — the works.

Even with all of that, it took a $100K cut and three months to get a buyer. The combination signal here is the same as Nantucket: if you're selling at the top of the Costa Mesa ADU market, you need to price at the comp from day one. The market is not going to chase you. For sellers walking into this market, the pre-listing prep work matters more than ever.

What this means for buyers.

The bifurcation is your opportunity. Two distinct strategies are working right now:

Strategy 1 — Buy permits, not finishes. 934 Governor was the cleanest play of the quarter. The buyer paid $1.4M for a property where the permitting work had already been done, and they'll capture the construction margin themselves. If you're an investor with a builder on call, this is where the alpha is in Costa Mesa right now. Watch for properties listing with "approved plans" in the description — they're moving fast.

Strategy 2 — Wait at the top. If you want a turnkey $3M ADU home, the leverage has shifted to your side. Sellers in this band are negotiating. A property listed at $3.1M is realistically going to trade in the high $2.8s to low $2.9s after rate-of-time discovery. Don't pay original list. The Nantucket and 19th St comps both show cuts, and there's no urgency on the buy side at this tier.

Whichever strategy fits, run the detached vs. attached math before you buy — the cost-vs-rent equation in Costa Mesa is the cleanest argument for matching ADU type to lot.

What this means for sellers.

Two things, both of them blunt:

If your property has permits or an existing high-quality ADU, lead with that in the listing and price at the comp. The 934 Governor outcome — over asking, all cash, 12 days — is achievable. The buyer pool for ready-to-build property is thin but motivated.

If your property is a $3M turnkey ADU home, price under your gut feel and skip the price-cut dance. Both Nantucket and 19th St started high and had to cut. The market punishes that pattern with longer DOM and weaker final numbers. Get to the right number on day one.

A note on rental strategy: short-term rental income should not be in your underwriting for Costa Mesa. The city's short-term rental ban means an ADU here is a long-term rental play or a multigenerational play — not an Airbnb. Buyers underwriting accordingly are the only buyers serious sellers should be courting.

For city-specific permit and setback questions, Costa Mesa's ADU planning page is the source of truth, and California's HCD ADU rules define the state floor that Costa Mesa builds on top of. On the financing side, current Fannie Mae ADU income guidelines continue to recognize ADU rental income for qualifying — which keeps the buyer pool for permits-in-hand properties healthy heading into summer.

Bottom line for May 2026.

The Costa Mesa ADU market is no longer a single market. The permits-and-plans tier is hot, the luxury turnkey tier is soft, and the gap between them is the most important pattern of the quarter. Underwrite for the tier you're actually in.

If you want a parcel-specific read on where your property fits, that's the conversation I have every week. Send me the address and I'll pull the comps.

Garden Grove ADU Market Update — May 2026: What's Active, What Closed, and What the Numbers Are Telling Us

The Garden Grove ADU market in May 2026 is doing something no other OC city is doing right now: producing fully-stacked SFR + ADU + JADU triplex configurations as the standard listing format. Almost every active listing this month has multiple income units already permitted on a single lot. The buyer pool — investor-heavy, multigenerational-family-heavy, cash-heavy — is showing up specifically for this configuration.

But the data also tells a sharper story underneath. Cash buyers are dominating closes. Below-asking discounts are common. And mispriced listings are getting punished hard — sometimes with $200K+ reductions before they close.

Here's the full breakdown across Garden Grove's neighborhoods.

What's Currently Active and Pending

A snapshot of the active and pending Garden Grove ADU inventory in May 2026:

Active Inventory ($1.19M – $1.79M):

12162 Fieldgate (92841) — $1,199,000 — 3-bed main + attached 2nd-story Junior ADU 500 sq ft (rented) — 1988 ADU build year, older permitted unit. 69 DOM.

13291 Fairview St (92843) — $1,349,000 — Reduced from $1,399,000. Two new homes on one lot — 925 sq ft front + brand-new 2026 detached ADU 3-bed/2-bath 1,200 sq ft with paid-off solar. 62 DOM.

14061 Parson St (92843) — $1,480,000 — Triplex producing $7,500/mo: Unit 1 ($3,700/mo), Unit 2 (749 sq ft built 2023, $2,750/mo), Unit 3 (added 1-bed/1-bath, $1,050/mo). 57 DOM.

9151 Carl Ln (92844) — $1,480,000 — Multi-family with main 3-bed/2-bath ($3,500/mo) + 1,100 sq ft detached ADU 3-bed/2-bath built 2021 ($3,400/mo). $6,900/mo combined. 65 DOM.

9642 Orangewood Ave (92841) — $1,650,000 — Price raised from $1,599,000. Two homes on a 12,632 sq ft lot (over 1/4 acre) — main 2,000 sq ft + 800 sq ft detached ADU built 2020. SB9 potential. Pool. 26 DOM.

9282 Marietta (92841) — $1,699,000 — Brand new on market 5/6. Three units on a 14,303 sq ft Nichols Manor corner lot — 4-bed main + upstairs Junior ADU + detached 693 sq ft ADU. 5 Garden Grove Beautification Awards.

13611 Glenhaven Dr (92843) — $1,728,000 (auction June 5) — Triplex producing $8,600/mo with 1,200 sq ft detached ADU built 2023 leased at $3,800/mo. 42 DOM.

11131 Mac Murray St (92841) — $1,799,000 — Reduced from $1,890,000 ($91K cut). 4-master-bedroom layout with separate entrances + new 2026 JADU. 62 DOM.

Pending (Already Under Contract):

12081 Bangor St (92840) — $1,199,000 — Pending in 19 DOM. ADU permitted and under construction (2026 build, 800 sq ft 2-bed/2-bath) + SB9 plans approved next. Buyer is acquiring the upside potential, not the finished product.

11246 Mac (92841) — $1,300,000 — Pending in just 4 DOM. Renovated main + new 2-bed/2-bath ADU built 2020 (799 sq ft) with separate utilities and address. Pool, spa, BBQ. The fastest move in the data.

11662 Stephanie Ln (92840) — $1,398,000 — Pending. Two units producing $6,995/mo: Main ($3,995/mo) + new 2022 ADU 2-bed/2-bath 800 sq ft ($3,000/mo). $694,500 per unit. 29 DOM.

What Actually Closed — And What the Closes Are Telling Us

This is where Garden Grove gets really interesting. The closed sales tell a sharper story than the actives.

The clean win: 13631 Hope (92843) — Listed at $1,495,000, closed at $1,495,000 in 24 days. Full asking. Fully remodeled main + permitted ADU + brand-new appliances + paid-owned solar + custom landscaping + vacant for showings. Conventional financing buyer with $39,900 in concessions. The seller priced it correctly, prepared it correctly, and the market rewarded both.

The fast cash play: 11552 West (92840) — Listed $1,200,000, closed $1,180,000 in 9 DOM. Front 4-bed renovated 2019 + brand-new 2022 ADU 2-bed/2-bath 780 sq ft ($2,500/mo rent). Cash buyer.

The below-asking grind:

10082 Bonser (92840) — Listed $1,350,000, closed $1,320,000 (18 DOM). Renovated main + 710 sq ft attached ADU. Cash buyer, $26,400 buyer broker concession.

11341 Jacalene (92840) — Listed at $1,020,000 (originally $1,075,000), closed at $1,000,000 (135 DOM). The slow grind — total reduction of $75K from original list, then closed $20K under final list. Conventional buyer.

The cautionary tale: 11222 Anabel Ave (92843) — Listed at $1,399,000 (originally $1,499,000), closed at $1,200,000 in 33 days on market. $299,000 total below original list price. This is what happens when a property is mispriced — the market tells you eventually, but it costs you nearly $300K to find out. Cash buyer.

The Five Things This Data Is Telling Us About Garden Grove

1. Garden Grove is California's standout multigenerational ADU market. Look at the active triplex configurations: 13611 Glenhaven (8 beds across 3 units), 14061 Parson (3 units producing $7,500/mo), 9282 Marietta (4-bed main + 2 ADUs), 11662 Stephanie (2 income streams), 9151 Carl (2 income streams), 9642 Orangewood (1/4 acre with separate ADU driveway). The Vietnamese-American buyer base is real and visible — it's driving the demand for stacked income-unit configurations that work for extended families AND investors at the same time.

2. Cash buyers are dominating Garden Grove ADU closes in May. Three of the five recent closes (Bonser, Anabel, West) closed with cash. That's a much higher cash percentage than what we saw in Anaheim or Long Beach. The implication: investors and multigenerational families with capital are bypassing the financing process to lock in Garden Grove deals fast. Sellers who price correctly close fast. Sellers who don't watch their property turn into a $200K+ reduction story.

3. The fast-movers all share three traits. 11246 Mac (4 DOM, pending) and 13631 Hope (24 DOM, closed full ask) both had: realistic pricing, brand-new permitted ADUs (2020+ build), and clean documentation. Bangor St (19 DOM, pending) added a fourth differentiator — upside in the form of an ADU under construction plus SB9 plans approved. Buyers in this market are pricing the future, not just the present. I broke the same dynamic down in why ADU properties stall on the market.

4. Below-asking is the norm, not the exception. Look at the closed-vs-list spreads: Anabel -$199K from final list (-$299K from original), Jacalene -$20K, Bonser -$30K, West -$20K. The only at-asking close was Hope. This is meaningfully different from Anaheim's market where at-asking and over-asking sales were more common. Garden Grove buyers are negotiating harder, and sellers who anchor too high are paying the cost.

5. Brand-new 2020+ ADU construction is the standard now. Look at the build years on the inventory: 2020 (Mac, Orangewood, Hope, Stephanie's 2022 detail), 2021 (Carl), 2022 (West, Stephanie), 2023 (Glenhaven, Parson), 2026 (Fairview, Mac Murray, Bangor under construction). Garden Grove's city ADU program and ADU Go pre-approved plans are doing real work. Older 1980s/1990s ADU builds (like the Junior ADU at 12162 Fieldgate, built 1988) are now the outliers.

Garden Grove Sub-Market Notes

West Garden Grove / Nichols Manor (Area 62, 63 — west of Euclid): Premium pocket. Inventory ranges from $1.299M (12162 Fieldgate) up to $1.799M (Mac Murray). Larger lots more common — 9282 Marietta on 14,303 sq ft, 9642 Orangewood on 12,632 sq ft. SB9 potential mentioned multiple times. Owner-occupants with income strategies are the dominant buyer.

Garden Grove E of Euclid / W of Harbor (Area 64): Mid-tier inventory $1.0M–$1.4M. The cash-buyer-grind area where Anabel and Jacalene closed. Investor-heavy demand, more aggressive negotiation, slower close timelines on mispriced listings. Multigenerational family demand is strong here.

N of Bolsa / S of Garden Grove / E of Brookhurst (Area 66): Some of the strongest closes — 13631 Hope at full ask in 24 days. Newer renovations, well-priced inventory moves fast. The auction at 13611 Glenhaven (June 5) is a non-standard sale but reflects how active this corridor is.

Orange & Garden Grove area (Area 72) / Santa Ana North of First (Area 70): Border pockets with new construction visible. 12081 Bangor with ADU under construction + SB9 pipeline pending in 19 days. 13291 Fairview with brand-new 2026 ADU and paid solar.

Garden Grove's ADU Permitting Edge

One reason Garden Grove sees so much new ADU construction is the city's well-developed permitting pipeline. The City of Garden Grove ADU program lays out clear rules, and the ADU Go pre-approved plan program gives owners a real shortcut — four pre-reviewed, pre-approved, code-compliant ADU plans available for free. For Garden Grove buyers planning to add an ADU to an existing property, this is a real cost and timeline saver.

The local rules sit in Chapter 9.54 of the Garden Grove Municipal Code, which mirrors most of California's state ADU framework from HCD and adds local setback, height, and lot coverage specifics. The Garden Grove ADU FAQ is the quick-reference doc most homeowners actually read.

For sellers with older unpermitted units — and Garden Grove has a high concentration of these from decades of multigenerational housing — California's AB 2533 legalization pathway lets you bring pre-2020 units into compliance without penalties. This can be the $100K–$200K swing between a sale that maxes out and one that follows the Anabel pattern.

What Garden Grove's Build-Year Sweet Spot Is Telling Us

The pattern across active and closed inventory is consistent: older home (1951–1959) + brand-new ADU (2020–2026). Almost every quality property in May 2026 follows this template. The implication for buyers and sellers is the same — older Garden Grove housing stock with newly added permitted ADUs is what the market wants. Properties without an ADU are at a disadvantage. Properties with an unpermitted ADU need a clear AB 2533 plan. Properties with a brand-new permitted ADU + clean documentation are the ones moving fast.

This matters because Garden Grove's housing stock is largely 1950s-built ranch homes — the perfect candidates for ADU additions. The lot sizes (often 7,000–10,000+ sq ft) support the build. The state law guarantees the buildability. The city's pre-approved plans shorten the timeline. And the buyer demand is there for the finished product. Every piece of the chain works.

What This Means If You're a Buyer in Garden Grove Right Now

The opportunity zones depend on your strategy:

Cash investor: The $1.0M–$1.35M range with existing permitted ADU income. The Bonser, Anabel, and West closes show this is the active negotiation zone. Be patient and disciplined — Garden Grove sellers in this tier are accepting below-list offers when the cash is real.

Multigenerational family: Premium pocket triplex configurations like 9282 Marietta or 13611 Glenhaven. These work because everyone gets their own unit and their own entrance, but you keep the family compound feel. The lifestyle premium is real.

House-hacker: Look for the $1.2M–$1.4M stacked SFR + ADU listings. With Fannie Mae's projected ADU rent qualification, you can use the ADU income to qualify for the loan, live in the main house, and have the ADU offset your mortgage substantially. Stephanie Ln pending at $1.398M is the model.

Upside hunter: Properties with ADUs under construction or SB9 plans approved (like 12081 Bangor) are priced at the present value but include real upside as those units come online. Bangor went pending in 19 days for a reason — the upside is the product.

What This Means If You're a Seller in Garden Grove Right Now

Three things drive the strongest sale outcomes in May 2026:

1. Realistic pricing backed by the actual comp data. The Anabel grind ($299K below original) and the Mac Murray $91K reduction are textbook examples of pricing too high in a market that doesn't reward it. I broke down the full pricing framework in what your home with an ADU is actually worth.

2. Quality presentation and clean permits. Hope closed at full asking partly because it was vacant, fully renovated, and had a permitted ADU with paid-owned solar. That clarity drives buyer confidence and competing offers. I covered why this matters in how a home with an ADU is valued when you sell.

3. Tenant strategy locked in before listing. Many Garden Grove properties have tenants in place producing strong rent. That can help (clean rent rolls for investor buyers) or hurt (below-market rents discount your sale price). I covered the framework in whether to sell vacant or with tenants in place. For Garden Grove specifically, vacant properties (like Hope, like 11552 West) tend to attract the strongest cash offers.

The Bottom Line

Garden Grove's May 2026 ADU market is genuinely different from Anaheim's or Long Beach's. The cash buyer percentage is higher. The triplex configurations are more common. The multigenerational family demand is the strongest in OC. And the discipline required from sellers is unforgiving — price right and you close fast, price wrong and you watch a $200K+ reduction unfold over months.

If you want to talk through a specific Garden Grove property — buying or selling — that's exactly what I do. Let's go through the numbers together.

Book a Free ADU Strategy Session

For sellers specifically: Get the Free ADU Seller Kit

For more on the Garden Grove market overall: Garden Grove ADU Market Page

Dylan Serna is an Orange County Realtor (DRE# 02217359) with eXp Realty specializing in ADU and investment real estate. Learn more at adurealtor.net.

Long Beach ADU Market Update — May 2026: What's Active, What's Sitting, and What the Data Is Telling Us

The Long Beach ADU market in May 2026 is doing something almost no other Southern California market can match right now: producing brand-new ADUs at scale across every price tier and every neighborhood. Long Beach is California's per-capita ADU leader for a reason, and the May inventory makes that lead obvious.

But the same data tells a sharper story underneath the surface. The right ADU property at the right price is moving fast — sometimes in under two weeks. The wrong price or the wrong positioning, and you're sitting at 100+ days on market with multiple price reductions.

Here's the full breakdown across Long Beach's neighborhoods.

Long Beach's Active ADU Inventory by Price Tier

The May 2026 active ADU inventory in Long Beach is unusually deep. A few things to highlight before the neighborhood breakdowns:

Entry Tier ($770K–$1.05M):

2676 Golden, Wrigley (90806) — $770,000 — Brand new on market 5/4. Fixer. 3-bed main + 500 sq ft ADU. Doesn't qualify for FHA or VA — only renovation loans (FHA 203k, Fannie Mae renovation, etc.). The cheapest entry price in Long Beach right now, but you're buying a project.

1029 Maine Ave, Willmore District (90813) — $799,900 — Historic 1914 Craftsman + 400 sq ft 2-bed/1-bath detached ADU. Rent Control disclosed.

2911 Baltic, Wrigley (90810) — $826,000 — 3-bed main + permitted 1-bed ADU 360 sq ft. 112 days on market.

2033 W Burnett St, Westside (90810) — $849,900 — Brand new on market 5/1. Brand-new 2024 detached 2-bed/2-bath ADU 780 sq ft + remodeled front home. Both units rented.

161 W Harcourt St, North Long Beach (90805) — $899,999 — Reduced from $949,999. Permitted attached studio ADU 403 sq ft. 44 DOM.

6147 Gundry, North Long Beach (90805) — $1,050,000 — 1927 Spanish-style + permitted 2023 standard ADU (1 bed, $2,000/mo rent) + 2021 Junior ADU (studio, $1,000/mo). Triple-income property.

Mid Tier ($1.04M–$1.4M):

1835 E Florida St, Alamitos Beach (90802) — $1,049,000 — Brand new 5/5. Updated 1919 Craftsman + studio ADU rented at $1,250/mo. 3 DOM — already moving fast.

757 N Loma Vista, Willmore (90813) — $1,150,000 — Reduced from $1,350,000 ($200K cut). 1903 duplex with permitted ADU. 88 DOM.

1901 N Bellflower Blvd, Los Altos (90815) — $1,243,000 — Coming Soon, showings start 5/16. Brand-new 2026 detached studio ADU + remodeled main + paid solar + EV-ready.

1131 E 21st, Poly High (90806) — $1,299,990 — Reduced from $1,399,000. Two brand-new 2026 ADUs (Junior ADU + Standard) on a renovated 1929 main.

1416 Orange, Cambodia Town (90813) — $1,299,999 — 141 DOM. Triplex configuration with main + large 1,600 sq ft attached ADU (3 bed/4 bath).

456 Cherry Ave, Retro Row/Alamitos Beach (90802) — $1,375,000 — Reduced from $1,399,500. 1912 Craftsman + 750 sq ft ADU built 2023. 64 DOM.

5840 E Oakbrook, Los Altos (90815) — $1,379,000 — Brand new 5/7. Watson Brothers renovation + permitted detached ADU built 2020. Corner lot.

3246 N Marwick, South of Conant (90808) — $1,390,000 — Active Under Contract 5/6 (35 DOM). Renovated 2023 main + ADU garage conversion + heated pool.

3945 Gondar Ave, Carson Park (90808) — $1,399,000 — Designer renovation + ADU. Seller disclosed ADU is unpermitted.

774 Gladys, Rose Park (90804) — $1,399,000 — Active Under Contract in 10 DOM. 1919 Craftsman + permitted 2024 ADU + Mills Act for huge tax savings.

Premium Tier ($1.49M–$2.15M):

2151 Euclid Ave, Artcraft Manor (90815) — $1,499,000 — Reduced from $1,525,000. Two new construction 2026 ADUs + remodeled main. 70 DOM.

4851 Faculty, Lakewood Village (90808) — $1,595,000 — Permitted ADU + Jr. ADU both built 2023.

5339 E Greenmeadow, Lakewood Village (90808) — $1,675,000 — Reduced from $1,735,000 (60 DOM). Permitted 2025 ADU 362 sq ft. Room for additional ADU + pool.

234 Lindero Ave, Bluff Heights Historic (90803) — $1,695,000 — Brand new 5/6. Restored 1913 Craftsman duplex + 384 sq ft ADU. Sellers have no permit records for the existing improvements.

3711 Lemon, California Heights (90807) — $1,800,000 — Three-residence triplex on three parcels (~10,000 sq ft total). $1,158/mo + $2,055/mo current rents.

4529 Pepperwood Ave, Lakewood Village (90808) — $2,149,900 — 6-bed main with 3 primary suites + brand-new 2025 detached ADU. 29 DOM.

Top Tier ($3.15M+):

4217 Cedar, Virginia Country Club (90807) — $3,149,000 — Brand new 5/7. Kenneth Wing-designed 1956 estate + small detached ADU casita. "Lowest price per sq ft amongst the Estate homes in Virginia Country Club."

5401 E El Parque, Park Estates (90815) — $3,895,000 — Designer-renovated mid-century with heated pool + 616 sq ft ADU. Back on market after a previous deal fell through. 42 DOM total.

What the Data Is Telling Us About Long Beach

1. Long Beach is genuinely producing more ADUs than any other OC/LA market. Look at the build years on active inventory: 2021, 2023, 2023, 2024, 2025, 2025, 2026, 2026, 2026. Brand-new construction ADUs aren't a rare feature here — they're the norm. The City of Long Beach's Pre-Approved ADU Program (PAADU) and streamlined building department processes are exactly why you see this volume — Long Beach is a city built around making ADU construction easier, and the inventory reflects it.

2. The Mills Act is a real differentiator at the historic-tier price points. Look at 774 Gladys in Rose Park — it went under contract in 10 days at $1.399M. The Mills Act enrollment alone is worth thousands per year in property tax savings. When a historic Long Beach Craftsman has a permitted ADU AND the Mills Act, the buyer pool widens dramatically and the deal closes fast. Same dynamic I broke down on the Anaheim side with the historic Hensley House sale.

3. Triplex stacking is standard play in Long Beach. Look at 4851 Faculty (3 units in Lakewood Village), 3711 Lemon (3 residences in Cal Heights), 6147 Gundry (3 units in North LB), 1131 E 21st (3 units in Poly High), 1416 Orange (3 units in Cambodia Town), 2151 Euclid (3 units in Artcraft Manor). Long Beach is one of the few SoCal markets where the SFR + ADU + JADU stack is so common it almost feels expected. The buyer pool for these is investor-heavy, but multigenerational families show up too — especially in the more residential pockets.

4. The market is punishing mispriced listings hard. 1416 Orange at 141 DOM. 2911 Baltic at 112 DOM. 757 N Loma Vista at 88 DOM with a $200K reduction. 5339 Greenmeadow with a $60K cut. 161 W Harcourt with a $50K cut. 1131 E 21st with a $99K cut. 2151 Euclid with a $26K cut. The pattern is clear: when a Long Beach ADU property doesn't pencil at the original list price, buyers wait it out. I broke down the full pricing trap in why ADU properties stall on the market. Long Beach is no different from OC — the math has to work for the buyer pool that's actually active.

5. Fast-moving listings have a clear pattern. 774 Gladys (10 DOM, under contract), 1835 E Florida (3 DOM, momentum heavy), 3246 N Marwick (35 DOM, under contract). The fast-movers all share traits: realistic pricing, quality finishes, permitted ADUs (or the Mills Act in lieu of), and clean documentation. The slow-movers have one or more of these missing.

6. Unpermitted ADU disclosures are showing up across multiple listings. 3945 Gondar (seller disclosed unpermitted ADU), 4357 Sunfield (city previously forced kitchenette removal), 234 Lindero (sellers have no permit records), 4357 Sunfield. For these properties, the buyer needs a clear plan — legalize under California's AB 2533 pathway or build a new permitted detached ADU. The presence of unpermitted units doesn't kill a deal, but it changes the math meaningfully.

Long Beach Sub-Market Notes

Lakewood Village (90808) — The ADU Activity Capital. More active ADU inventory than any other Long Beach pocket. Active listings here run from $1.35M (4357 Sunfield) to $2.15M (4529 Pepperwood). Premium price tier, mid-century housing stock from 1939–1954, and a steady flow of brand-new permitted ADUs being added to renovated mains. The buyer pool here is owner-occupant and house-hacker heavy — people who actually want to live in this neighborhood.

Los Altos (90815) — Premium with CSULB Tenant Pool. Active inventory $1.24M–$1.7M. Watson Brothers Fine Homes is showing up as a recurring renovator (5840 Oakbrook). Cal State Long Beach proximity means strong rental demand for any ADU here. The 1901 N Bellflower property coming on the market 5/16 is a great example of the standard play — main home + brand-new 2026 ADU + paid solar.

Bixby Knolls / California Heights / Virginia Country Club (90807) — Premium Money. $1.8M (3711 Lemon triplex) up to $3.149M (4217 Cedar VCC estate). The buyer pool here skews toward owner-occupants and multigenerational families with budgets to match the prices. ADU comes as a bonus, not the lead feature.

Park Estates (90815) — Designer-Forward Top Tier. 5401 E El Parque at $3.895M is the headliner — sitting on a 15,891 sq ft corner lot with a fully equipped ADU. Limited inventory, premium pricing, longer days on market because the buyer pool at this price point is small.

Belmont Heights / Bluff Heights / Eastside (90803, 90804) — Coastal Historic. Bluff Heights Historic District (234 Lindero, $1.695M restored 1913 Craftsman). Rose Park (774 Gladys, $1.399M with Mills Act, under contract in 10 days). These are some of the strongest niches for the right buyer — historic charm + ADU income + sometimes Mills Act tax savings.

Alamitos Beach / Retro Row / Downtown (90802) — Walkable Coastal Lifestyle. 1835 E Florida ($1.049M, 3 DOM). 456 Cherry Ave ($1.375M, 64 DOM). The lifestyle premium is real here — walkable to Retro Row, coffee shops, the shoreline. Smaller lots and ADUs make the math tighter, but the lifestyle pull keeps demand consistent for the right properties.

Willmore District / Cambodia Town (90813) — Downtown Value. 1029 Maine ($799,900), 757 N Loma Vista ($1.150M after $200K cut), 1416 Orange ($1.299M, 141 DOM). Older housing stock (1903–1941), opportunistic pricing, but the buyer pool is more cautious — partly because of rent control disclosures and zoning complexity.

North Long Beach (90805) — The Value Pocket. 161 W Harcourt ($899,999), 6147 Gundry ($1.05M with two permitted ADUs producing $3,000/mo total). Lowest entry price for properties with real ADU income already in place. Investor-heavy buyer pool. The pocket I covered in detail in why North Long Beach is the LA County ADU market new investors should be in right now.

Wrigley / Westside (90806, 90810) — The Sub-$1M Tier. 2676 Golden ($770K fixer), 2911 Baltic ($826K with permitted ADU, 112 DOM), 2033 W Burnett ($849,900 with new construction ADU). These are the lowest-entry-price plays in Long Beach proper. Tight lots, smaller homes, but the math works if you're patient and selective.

Long Beach's ADU Permitting Edge

One reason Long Beach moves so much ADU inventory is the city's well-developed permitting infrastructure. The City of Long Beach ADU department processes more ADUs per capita than any other city in California, and the PAADU pre-approved plan program gives buyers a real shortcut for new builds.

For investors looking at properties with unpermitted units — common across Long Beach's older Wrigley, Willmore, and North LB stock — California's AB 2533 legalization pathway lets you bring pre-2020 units into compliance without penalties. This applies to LA County properties just like OC.

These local resources sit on top of the state framework from California HCD, which keeps Long Beach's by-right ADU buildability protected even as local rules continue to evolve.

The Build-Year Sweet Spot Is Different in Long Beach Than in Anaheim

In Anaheim, the sweet spot is older home (1949–1965) + recent ADU (2018–2025).

In Long Beach, the pattern is similar — but Long Beach has a much higher concentration of brand-new 2024–2026 ADU builds. This matters for two reasons:

Buyers don't have to wait. A buyer of 2151 Euclid or 1131 E 21st gets a fully permitted, brand-new, ready-to-rent triplex setup on day one. No 12+ month construction timeline.

Resale comp data is improving fast. Every new ADU build that closes adds to Long Beach's already-deepest-in-California ADU comp pool. By the time today's brand-new construction hits resale in 5–10 years, the comp data will be exceptional.

The implication: if you want maximum cash flow on day one and you don't want to manage a build project yourself, Long Beach's brand-new construction inventory is genuinely the strongest in OC/LA right now. If you'd rather build your own (and capture the construction-cost-to-value spread), the older housing stock in North LB and Wrigley gives you the best entry price for that play.

What This Means If You're a Buyer in Long Beach Right Now

The opportunity zones depend on your strategy:

Pure cash flow investor: North LB and Wrigley at $850K–$1.05M with existing permitted ADU income. The 6147 Gundry play (2 ADUs producing $3,000/mo on a $1.05M property) is a model.

House-hacker: Lakewood Village or Los Altos. Buy a property with a brand-new 2024–2026 ADU, live in the main, rent the ADU, let the income offset the mortgage. Use the Fannie Mae projected rent rule to qualify.

Lifestyle owner-occupant: Belmont Heights, Bluff Heights, Rose Park, or Alamitos Beach. Pay the lifestyle premium, get Mills Act savings if you can, and let the ADU subsidize the cost of being in the neighborhood you actually want to live in.

Value play with renovation budget: Wrigley, Westside, or downtown at $770K–$900K. Be honest about your renovation and ADU build budget before you commit. The cheapest entry price doesn't always pencil.

What This Means If You're a Seller in Long Beach Right Now

The market is selective. Three things are driving the strongest sale outcomes in May 2026:

1. Realistic pricing backed by Long Beach ADU comp data. With Long Beach producing more ADU comps than any other city in California, the data exists to defend a strong price — but it also exists to expose an aggressive one. I broke down the pricing framework in what your home with an ADU is actually worth.

2. Clean permits and documentation. Properties with vague or missing permit records are sitting longer. 234 Lindero ("sellers have no permit records") is a $1.7M property with a permit cloud over it — that uncertainty is doing real work in extending DOM.

3. Tenant strategy locked in before listing. Properties with month-to-month tenants and clean rent rolls (3711 Lemon with documented $1,158 + $2,055 rents) are easier for investor buyers to underwrite. Below-market or unclear tenant situations create friction. I covered the framework in whether to sell vacant or with tenants in place.

The Bottom Line

Long Beach's May 2026 ADU market has more inventory, more brand-new builds, and more sub-market variation than any other OC/LA city. That depth is an advantage for buyers who know exactly what they're looking for — and a challenge for sellers who don't price and position for the buyer pool that's actually active in their specific pocket.

The fast-movers (3, 10, 12, 35 days on market) all share the same traits: priced for the real comp data, well-documented, well-finished. The slow-movers (88, 112, 141 days) all share the opposite. Long Beach rewards discipline.

If you want to talk through a specific Long Beach property — buying or selling — that's exactly what I do. Let's go through the numbers together.

Book a Free ADU Strategy Session

For sellers specifically: Get the Free ADU Seller Kit

For more on the Long Beach market overall: Long Beach ADU Market Page

Dylan Serna is a Realtor (DRE# 02217359) with eXp Realty specializing in ADU and investment real estate across Orange County and LA County. Learn more at adurealtor.net.

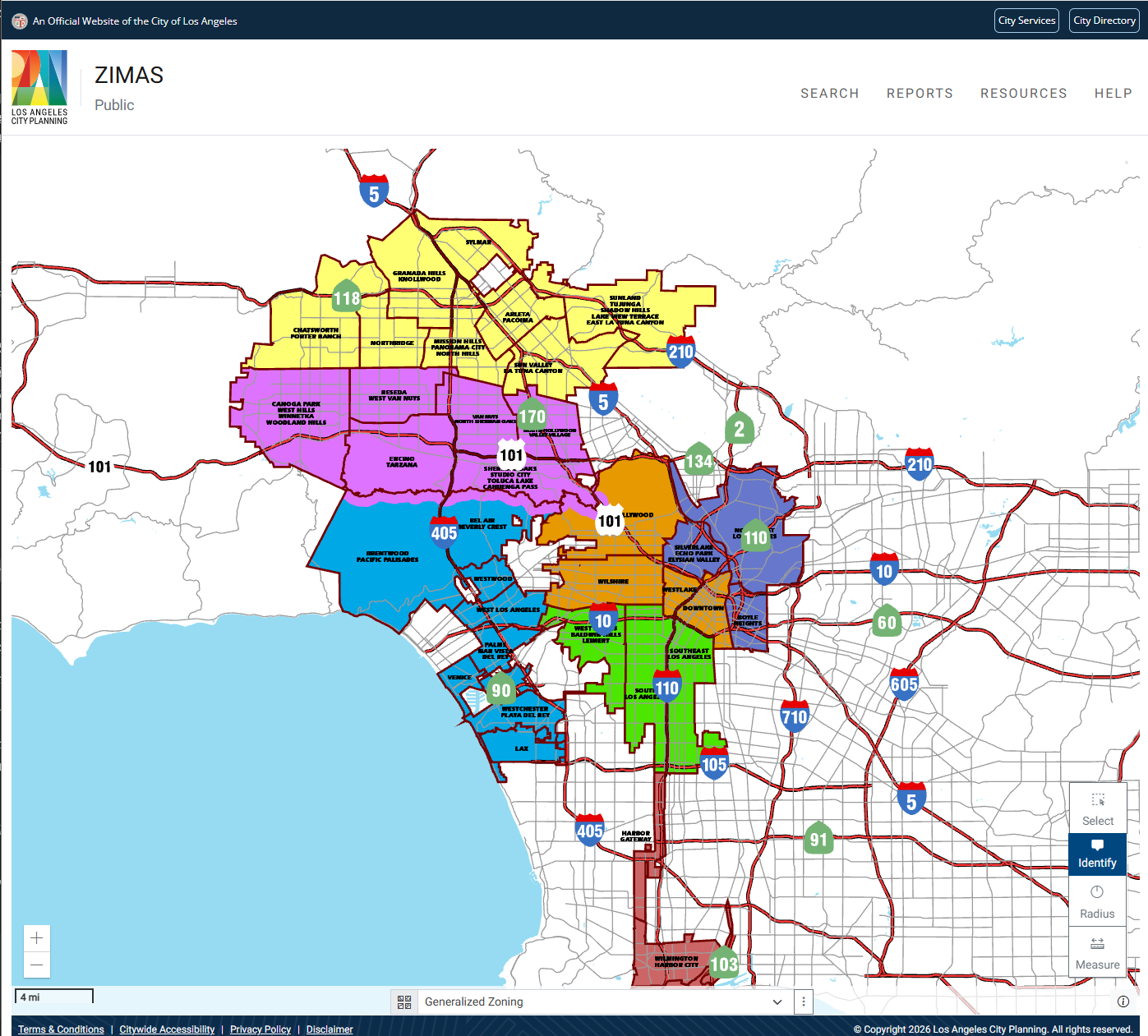

Most LA Investors Get Into Escrow Before Checking SB9 Eligibility — Here's the Free 60-Second Fix

If you're looking for SB9 opportunities in Los Angeles, ZIMAS is the first tool you need to learn. It's free, it's public, and it tells you in about sixty seconds whether a property qualifies for Senate Bill 9 — before you ever write an offer.

Most investors skip this step. They find a property they like, get into escrow, and then discover the lot doesn't qualify. That's a waste of everyone's time. Here's how to avoid it.

What Is ZIMAS?

ZIMAS (Zoning Information and Map Access System) is the City of Los Angeles's free online zoning tool. It lets you search any property in the city and pull up its zoning designation, overlays, specific plan areas, and — most importantly for our purposes — its SB9 eligibility status.

Think of it as the property's zoning report card. You type in an address, and ZIMAS tells you everything the city knows about what you can and can't build there.

Why SB9 Eligibility Matters Before You Buy

SB9 allows you to add a second primary unit onto a single-family lot — and unlike an ADU, that second unit is valued as a primary residence, not an accessory. That distinction matters at appraisal and resale.

But not every single-family lot qualifies. The property has to meet specific criteria under state law, and the fastest way to check is ZIMAS.

Step-by-Step: How to Check SB9 Eligibility on ZIMAS

Step 1: Go to ZIMAS

Open your browser and navigate to zimas.lacity.org. You'll see a map of Los Angeles with a search bar at the top.

Step 2: Search the Property Address

Type in the full street address of the property you want to check. ZIMAS will zoom into the parcel and display a summary panel on the left side of the screen.

Step 3: Open Planning and Zoning

In the left-side panel, look for the section labeled Planning and Zoning. Click to expand it. This is where the city stores all the zoning overlays, specific plans, and eligibility flags for the property.

Step 4: Find "SB 9 Eligibility"

Scroll down within the Planning and Zoning section until you see SB 9 Eligibility. Next to it, there's a View link. Click it.

Step 5: Read the Checklist

ZIMAS will display a checklist with four to five criteria. Each one will show a yes or no answer. The checklist covers:

Zoning designation — The property must be in a single-family residential zone. In the City of Los Angeles, the eligible zones are A1, A2, RA, RE, RS, R1, RU, RZ, and RW. If the property sits in R2, RD, C1, M1, or any other zone, it does not qualify.

Transit proximity — The property must be within half a mile of a major transit stop or a high-quality transit corridor.

Hazard zones — The property cannot be in a protected hazard area such as wetlands or a floodway. Note that properties in a Very High Fire Hazard Severity Zone or earthquake fault zone may still qualify depending on the specific overlay.

Historic designation — Properties listed in the State Historic Resources Inventory, designated as a Historic Cultural Monument, or located within a Historic Preservation Overlay Zone (HPOZ) are not eligible.

If every criterion passes, the property qualifies for SB9 development. If even one fails, it does not.

What to Do After ZIMAS Says "Yes"

A passing ZIMAS checklist means the property is eligible — but it doesn't mean you should automatically buy it. You still need to evaluate the deal the same way you would any ADU investment property: lot size, site plan feasibility, rental income projections, and total capital required.

Here's my recommended sequence after confirming SB9 eligibility:

Run the rent comps. Don't use the listing agent's projected income. Pull actual rents from the same neighborhood. When I evaluated an SB9 property on Hedda Street in Lakewood, the listing projected $12,800 per month. The real comps came in closer to $11,200 — a $1,600 per month difference that completely changes the cap rate math.

Check which SB9 path makes sense. There are two options: SB9 with a lot split and SB9 without a lot split. The lot split version requires you to intend to reside in one of the units for at least three years and typically takes about a year to process. The no-lot-split version keeps the parcel intact and usually takes around six months. If you want to understand how this pairs with ADUs, the City of LA memorandum (ZA Memo 143) lays out how combining SB9 with ADUs can get you up to four units on a single lot.

Get a feasibility report during escrow. I always have my ADU designer pull a feasibility study before we close so we know exactly what's buildable. This is especially important with SB9 because the unit placement, setbacks, and access requirements are stricter than a standard detached ADU build.

Common Mistakes Investors Make with ZIMAS

Assuming county properties work the same way. ZIMAS only covers the City of Los Angeles. If the property is in unincorporated LA County, you need to check LA County Planning's SB9 page instead. Different jurisdiction, different process.

Ignoring the hazard overlays. A property can sit in a single-family zone and still fail SB9 eligibility because of a wetland overlay or floodway designation. Always check every line of the checklist, not just the zoning.

Skipping the income verification. ZIMAS tells you if you can build. It doesn't tell you if you should. I've seen investors get excited about SB9 eligibility on a property where the numbers don't pencil out once you run honest rent comps. The income approach is how appraisers value these properties, and inflated projections will catch up with you at resale.

The Bottom Line

ZIMAS is the fastest free tool for checking whether a Los Angeles property qualifies for SB9. It takes sixty seconds, it's publicly available at zimas.lacity.org, and it should be the first thing you check before touring any potential SB9 investment property in the city.

If you're evaluating SB9 opportunities in LA and want help running the actual numbers — rent comps, cap rate analysis, and build feasibility — reach out on Instagram or grab my ADU Buyers Guide to get started.

North Long Beach: The ADU Pocket You Need to Buy Into Before Everyone Else Does

If you're looking at LA County for an ADU investment property — especially as a first-time investor trying to start a real portfolio — North Long Beach is the market you need to be looking at right now. The entry prices are still accessible, the city is one of the most ADU-friendly in California, and the deals that pencil today won't pencil at this price point much longer.

Long Beach is already the highest per-capita producer of ADUs in California, according to the City of Long Beach Community Development Department. That's not a fluke — it's the result of years of pro-ADU policy, strong rental demand from a renter-heavy population, and lot characteristics that genuinely support ADU construction. North Long Beach is the pocket inside that broader market where the entry-price math still works for new investors.

Here's the full breakdown.

The North Long Beach Entry Price Advantage

This is the headline. North Long Beach is one of the only LA County markets where you can still buy:

Single-family homes in the $800K–$900K range

Small duplexes in the same $800K–$900K range depending on condition

Compare that to most of OC, where entry-level SFRs start around $1.2M and quickly climb. Compare it to Westside LA, where you can't touch a single-family home for under $1.5M. North Long Beach is the most accessible entry point into the LA metro for an ADU-focused investor.

That price difference is the whole game. When you're starting your portfolio, lower entry price means lower down payment, which means more dry powder for the ADU build itself. A 25% down payment on an $850K North Long Beach property is roughly $213K — versus $300K on a $1.2M Halecrest property in Costa Mesa. That $87K delta either reduces your cash-in-the-deal or funds a meaningful chunk of your detached ADU build.

This is exactly the underwriting framework I broke down in how experienced investors decide which properties are best for an ADU — your total project cost (purchase + ADU build) is what makes or breaks the deal, and North Long Beach is where that math is friendliest right now for a new investor.

Why This Is the Best LA County Pocket to Start a Portfolio

If I'm an investor building a real estate portfolio from scratch in LA County in 2026, I'm starting in North Long Beach. Here's why:

1. Cash flow with a lower down payment is actually possible. At $850K with the SFR renting in the $3,200–$3,500/month range, you can structure 25–30% down and get the main house close to break-even on PITI without putting a massive amount of cash on the table. Add a detached ADU producing $2,400–$2,700/month in long-term rent, and the property pays you to own it.

2. The dual-asset opportunity (SFR + duplex options). Most ADU markets only give you single-family options. North Long Beach gives you both — small duplexes are available in the same entry-price band, which means you can get a 2-unit property and add an ADU for a true 3-unit income setup on one lot. That's portfolio acceleration most cities can't match.

3. Long Beach is a proven ADU city. With Long Beach being California's per-capita ADU leader, the city's building department actually knows how to process these projects. Permitting timelines are more predictable than in cities that handle 5 ADU permits a year. The city also offers a Pre-Approved ADU Program (PAADU) that further shortens timelines for buyers willing to use city-approved plans.

4. State law backstop. Long Beach currently applies California state ADU law directly while local ordinance updates work through the system. That means you get the full state-level homeowner protections — by-right ADU buildability, parking exemptions, setback minimums — on every property in the city.

5. Tenant pool is deep and consistent. Long Beach is a renter-majority city with steady demand from CSULB students, downtown workers, port-area workers, and LA-South Bay overflow tenants. North Long Beach specifically attracts working-class and young-professional renters who pay reliably and stay long-term when the unit is quality.

The Single Biggest ADU Tip for North Long Beach: Build New Detached. Don't Convert.

Here's the most important strategic decision you'll make on a North Long Beach property — and most new investors get it wrong.

Don't try to convert an existing structure into your ADU. Build a new detached unit instead.

The reason is the age of the housing stock. Most North Long Beach homes were built around 1940 — roughly 85+ years old. Conversions sound cheaper on paper because you're "just" reusing existing walls, foundation, roof, etc. But the ADU has to be built up to current code, not the code that was in place when the original structure went up.

When you bring a 1940 garage or back house up to current code, you're often dealing with:

Foundation that doesn't meet modern seismic and load requirements

Framing that doesn't meet current structural standards

Original electrical that has to be completely re-pulled

Plumbing that needs to be re-routed and brought up to current code

Insulation, fire separation, and energy compliance (Title 24) that didn't exist as standards in 1940

I've talked to multiple structural engineers about this exact scenario, and the verdict is consistent: bringing a 1940 structure up to current ADU code is often more expensive — and always more complicated — than building new. You strip the existing structure down to almost nothing, then rebuild it to current standards. At that point, you've spent conversion money and ended up with new construction anyway.

Compare that to a property built in the 1980s, where the underlying structure is much closer to current code already. There, an as-is conversion can save you significant money because you're not fighting decades of code drift. But North Long Beach isn't that market — the housing stock is too old.

The detached new-build path on a North Long Beach property gives you:

Predictable build costs (no surprise structural discoveries)

A modern unit that rents for top-of-market

Maximum resale value — both investors and owner-occupants pay the strongest premium for detached units, as I broke down in the 3 types of ADUs and why detached usually wins

Cleaner permit path through Long Beach's well-developed ADU process, which I covered the full sequencing of in how the ADU permitting and construction process works

This is the single most important strategic call on a North Long Beach property. Get it right and your deal pencils. Get it wrong and you're three months into a conversion realizing you should have just built new.

Pre-Purchase Tip: Check the Electrical Panel Before You Make an Offer

This is the property-level tip that saves more time, money, and headache than any other on a North Long Beach deal: check whether the electrical and main panel/sub-panel have been updated.

On a 1940-era home, the original electrical system is nowhere near sufficient to support both the existing main house load and a new ADU. You'll need to either upgrade the main panel or pull a separate service for the ADU — both of which cost real money and add real time to the project.

The properties where the previous owner already upgraded the panel save you:

$5K–$15K in panel upgrade costs

2–6 weeks of timeline waiting on the utility to schedule the upgrade

The hassle of coordinating the upgrade with construction

Permit complications from having to bring panel upgrades through inspection

Walk every property with this question in mind. Look at the panel. Ask the listing agent when it was last updated. If it's been done — that's a real, quantifiable advantage that should factor into how aggressive you can be on the offer. If it hasn't, build that cost and timeline into your underwriting from day one. Don't discover it post-close.

A Real North Long Beach ADU Math Example

Let's run the numbers on a typical North Long Beach SFR deal in 2026.

Buy a 3-bedroom SFR for $850,000. Put 25% down — that's $213K cash on a primary or investment loan, depending on whether you're house-hacking. The main house rents at $3,400/month, which roughly covers PITI on the remaining $637K loan plus taxes and insurance — close to break-even.

Build an 800 sq ft new detached 2-bedroom ADU at $350/sq ft (Long Beach build costs) — that's $280K in build cost. Total cash in the deal: roughly $493K all-in.

Rent the new detached ADU at $2,500/month (achievable in North Long Beach for a quality, modern unit). After property tax bump, insurance, and reserves, you net roughly $2,100/month in ADU cash flow.

That's ~$25K/year in cash flow on $493K invested — about 5% cash-on-cash, on top of:

Appreciation on a $1.13M all-in property in California's per-capita ADU capital

Principal paydown on the loan

~$200K–$400K in equity added by the permitted detached ADU itself

A property whose dual-income story will attract a strong investor buyer pool when you eventually sell

The fact that Fannie Mae now lets buyers count projected ADU rental income toward loan qualification means your eventual buyer pool — both investors and house-hackers — is wider than it has ever been. Long Beach's status as California's leading ADU city only strengthens that exit story.

Don't Sleep on the Duplex Plays

One thing that makes North Long Beach genuinely special: duplexes show up in the same $800K–$900K price band. That means you can buy a 2-unit property already producing rental income from both sides, and add a detached ADU for a 3-unit income property on a single lot.

The math on a duplex + ADU here is exceptional for portfolio building. You're buying two existing income streams plus adding a third. Cash flow stacks fast. Just keep in mind that duplexes built in the same 1940 era have the same conversion limitations as SFRs — build a new detached ADU on the lot rather than trying to add a unit by converting an existing structure.

Common North Long Beach ADU Mistakes I See

Trying to convert a 1940 garage to save money. As covered above — it's the most expensive "savings" move you can make. Build new detached. The math actually favors it once you account for code compliance.

Skipping the electrical inspection. Don't tour, write an offer, and discover post-close that you're staring down a $12K panel upgrade plus a 4-week utility delay. Check the panel during the showing.

Pricing the eventual sale off your construction cost. This trap shows up in every market, North Long Beach included. Buyers don't pay for your construction receipts — they pay for income, comps, and what the market supports today. I broke down the full pricing framework in how a home with an ADU is valued when you sell.

Buying on a lot that won't fit a real detached ADU. Some North Long Beach lots are tighter than others. If the only ADU option on a given property is a 500 sq ft junior unit, the cash flow math changes dramatically. Tour with someone who can evaluate the lot for actual buildability — not just guess from the listing photos.

Inheriting unpermitted units. A lot of older North Long Beach properties have garage conversions, back houses, or extra units that were never permitted. You need to know what you're buying and have a clear plan — legalize under California's AB 2533 pathway, or build a new permitted detached ADU instead. I walked through the legalization mechanics in how to sell a home with an unpermitted ADU. The same path applies to LA County properties — and it's especially relevant in a market this old.

What to Do Next

If North Long Beach is your market, the playbook is clear:

Lock in your full project budget before you tour. Purchase + ADU build + electrical/system upgrades + reserves. New investors who try to "figure it out as we go" lose money. Plan first.

Decide SFR or duplex. Both can work. Duplex accelerates portfolio cash flow faster, SFR is simpler operationally for a first deal.

Use the Long Beach Pre-Approved ADU Program if it fits your lot. It shortens permitting and reduces design fees substantially.

Walk the property with electrical and lot buildability in mind. These two checks during the showing prevent the most expensive surprises.

Move quickly on the right deals. North Long Beach prices are still accessible, but they're not staying there forever. The deals that pencil today are exactly why investors are going to be priced out of this market within the next few years.

If you want help finding the right North Long Beach property, evaluating it for ADU buildability, or running the numbers on a specific listing — that's exactly what I do. Let's talk.

Book a Free ADU Buyer Strategy Session

Or if you want a custom property search built around your North Long Beach ADU criteria: Customized ADU Property Search

For more on the Long Beach market overall: Long Beach ADU Market Page

Dylan Serna is a Realtor (DRE# 02217359) with eXp Realty specializing in ADU and investment real estate across Orange County and LA County. Learn more at adurealtor.net.

Eastside Costa Mesa: The Best Place to Live and Build an ADU That Actually Cash Flows

If you've spent any time in Costa Mesa, you already know Eastside is the lifestyle pocket of the city. Walkable, food-and-coffee-rich, minutes from Newport Beach, and full of the kind of mid-century cottage homes that buyers fall in love with on the first showing. It's one of the most desirable places to live in all of Orange County.

What most buyers don't realize is that Eastside is also one of the strongest cash-flow ADU markets in OC — but only if you understand how it works. The numbers don't pencil the way they do on Westside or in Halecrest, where lower entry prices do the heavy lifting. Eastside is a different play entirely. Here's why it works, who it works for, and how to actually build a deal that cash flows here.

Why Eastside Costa Mesa Commands Premium Pricing

Let's start with what you're paying for. Eastside Costa Mesa is roughly the area east of Newport Boulevard and south of the 55 freeway, anchored by the 17th Street corridor — one of the most walkable, food-and-coffee-dense commercial streets in Orange County. Eastside residents walk to grab coffee, walk to dinner, walk their dogs to the bars on Newport Boulevard, and bike to Back Bay or the beach in under 10 minutes.

That lifestyle is why Eastside trades at a premium. Single-family homes here run $1.8M–$2.5M+ depending on size, condition, and lot. The cottage homes near 17th Street and Orange Avenue can fetch top of the range when remodeled. The slightly larger homes deeper into the neighborhood — toward the Mesa del Mar border — hold value just as well.

This is the most desirable Costa Mesa pocket for owner-occupants, which means it's the most desirable Costa Mesa pocket for the kind of buyer who's going to pay you the strongest price when you eventually sell.

The Eastside ADU Rental Advantage — This Is Where the Cash Flow Lives

Here's what most ADU investors don't realize about Eastside: the rental rates here are dramatically higher than the rest of Costa Mesa.

A 2-bedroom detached ADU that rents for $3,000/month in Halecrest can rent for $3,800–$4,500/month on Eastside. A high-end 1-bedroom detached unit with quality finishes near 17th Street can push $3,500/month all by itself. The reason is the tenant pool — Eastside attracts:

Young professionals priced out of Newport Beach who still want the lifestyle and are willing to pay near-Newport rents to get it.

Newport Beach overflow tenants who want walkability, beach proximity, and quality finishes without the Newport price tag.

Couples and small families who specifically want a detached unit (not a condo, not an apartment) in a walkable pocket.

Remote workers who can live anywhere and choose Eastside for the lifestyle.

This tenant pool doesn't price-shop the way budget renters do. They want quality, they want location, and they pay accordingly. Build a quality detached ADU on Eastside and you're not competing with the broader OC rental market — you're competing with Newport Beach rentals at half the cost. That gap is where the cash flow lives.

The Lot Reality — Smaller, But Workable

Eastside lots are generally smaller than what you find on Westside, and noticeably smaller than the bigger Halecrest corner lots. A typical Eastside SFR lot runs roughly 5,000–6,500 sq ft, which is tighter than the rest of Costa Mesa.

That means a few things for ADU investors:

You'll typically build in the 700–1,000 sq ft range, not the full 1,200 sq ft maximum that Costa Mesa allows under the city's ADU ordinance.

Setbacks are tight. You'll need to design carefully to fit a detached ADU without variance. The state framework from California HCD sets baseline rules that protect ADU buildability, but Eastside's smaller lots mean every foot matters.

Garage conversions and JADUs become more attractive on the smallest Eastside lots. If you genuinely can't fit a detached ADU, a converted garage with proper permits can still produce strong rent — though detached almost always wins the resale battle, as I broke down in the 3 types of ADUs and why detached usually wins.

Lot selection is everything. The difference between a "this works" Eastside lot and a "this doesn't quite fit" Eastside lot is often a few hundred square feet of backyard depth. Tour with someone who knows what to measure before you write an offer.

The good news: the smaller ADU footprint isn't a deal-breaker on Eastside, because the per-square-foot rent here is so much higher than the rest of Costa Mesa. An 800 sq ft Eastside ADU at $3,800/month is producing more monthly income than a 1,200 sq ft Halecrest ADU at $3,000/month — same lot effort, better cash flow per square foot.

Why Eastside Is the Perfect House-Hacker Play

The buyer who wins on Eastside more than anyone else is the house-hacker — someone who's going to live in the main home, rent the ADU, and let the rental income offset the mortgage on a lifestyle home they actually want to live in.

The math here is genuinely powerful. You're not trying to make the property cash flow on day one as a pure investment. You're using the ADU to subsidize the cost of living somewhere you'd want to live anyway. And on Eastside, where the lifestyle is the whole point, that subsidy turns a $2M home from "out of reach" into "affordable when you factor in the ADU income."

The fact that Fannie Mae now lets buyers count projected ADU rental income toward loan qualification makes this even more powerful. You can use the projected $3,800/month ADU rent in your loan application — meaning you can qualify for an Eastside home you couldn't otherwise touch.

This is the same total-project-cost framework experienced investors apply, just from the owner-occupant side. I covered the underwriting logic in detail in how experienced investors decide which properties are best for an ADU — and Eastside is the city pocket where that logic produces a true win-win: live where you want, build the ADU that makes it possible, and bank the appreciation and equity over time.